Good morning and happy Sunday.

Tax alpha is critical and building tax-efficient portfolios and strategies is a better way to add alpha than trying to beat the market.

But first, a word from our sponsor, Northern Trust Asset Management.

Direct indexing is no longer just a tax strategy; it’s becoming a defining component of how leading advisors build and grow their practices.

As adoption has broadened, a clear divide has emerged. The real advantage today isn’t access to direct indexing but how effectively it’s implemented. A smaller group of advisors has gone beyond experimentation, embedding direct indexing into their core offering through personalized portfolios, ongoing tax benefits, and differentiated client experiences that drive growth.

New research from Northern Trust Asset Management explores this group of direct indexing “Superusers.” Based on surveys and interviews with advisors at high‑AUM firms, the research uncovers the behaviors, strategies, and decisions that set these advisors apart. For those assessing how direct indexing fits into their future, the insights offer a valuable roadmap.

How to Find Investing Insights from Tax Returns

Among the copious data advisors require from clients, tax returns are mission critical.

The documents are necessary to better design the plan, because taxes are fees, too, making tax alpha a priority. (While I’m still a licensed CPA, you don’t have to be one to find savings from tax returns.) The alpha from taxes is paramount because building tax-efficient portfolios and strategies is often a better way to add alpha than trying to beat the market. Here are six investing insights that can benefit clients:

Make the Most of Past Losses

Look to see if clients have a capital loss carryforward. With markets nearing all-time highs again, you’d think this would be fairly rare. It’s not, and clients regularly have huge tax-loss carryforwards. This provides two key insights. First, determine where the loss came from to shed light on possible poor behavior, such as panicking and selling during past market plunges. Many have said they buy in down markets only to have the tax return show otherwise. Understanding where the losses came from is critical in determining how much risk a client should take.

The second insight is that a loss carryforward opens possibilities to exit investments with high fees or those that are otherwise undesirable, such as expensive funds, or concentrated positions, while paying no taxes. (I jokingly tell the client: “I’m sorry for your loss, but let’s make the best of it.”) Estimate how much in the way of gains can be recognized without paying any federal income tax. That’s not to say that you should use all of it up because that loss carryforward has value for future years. Any unrealized losses can also be sold and used to offset gains or add to the tax-loss carryforward.

Understand Recognized Capital Gains and Dividends

Is the client recognizing capital gains and showing high dividend income? Sometimes this shows frequent trading but, more often than not, it’s due to being in tax-inefficient vehicles. When a mutual fund trades and recognizes a gain, it pushes out that gain to the client via a 1099. ETFs can almost always eliminate passing through gains via the creation and redemption process they use.

Also look at dividend income. That’s because total return is far more important than chasing dividends. Not only are they tax-inefficient (even qualified dividends) but they have also badly underperformed.

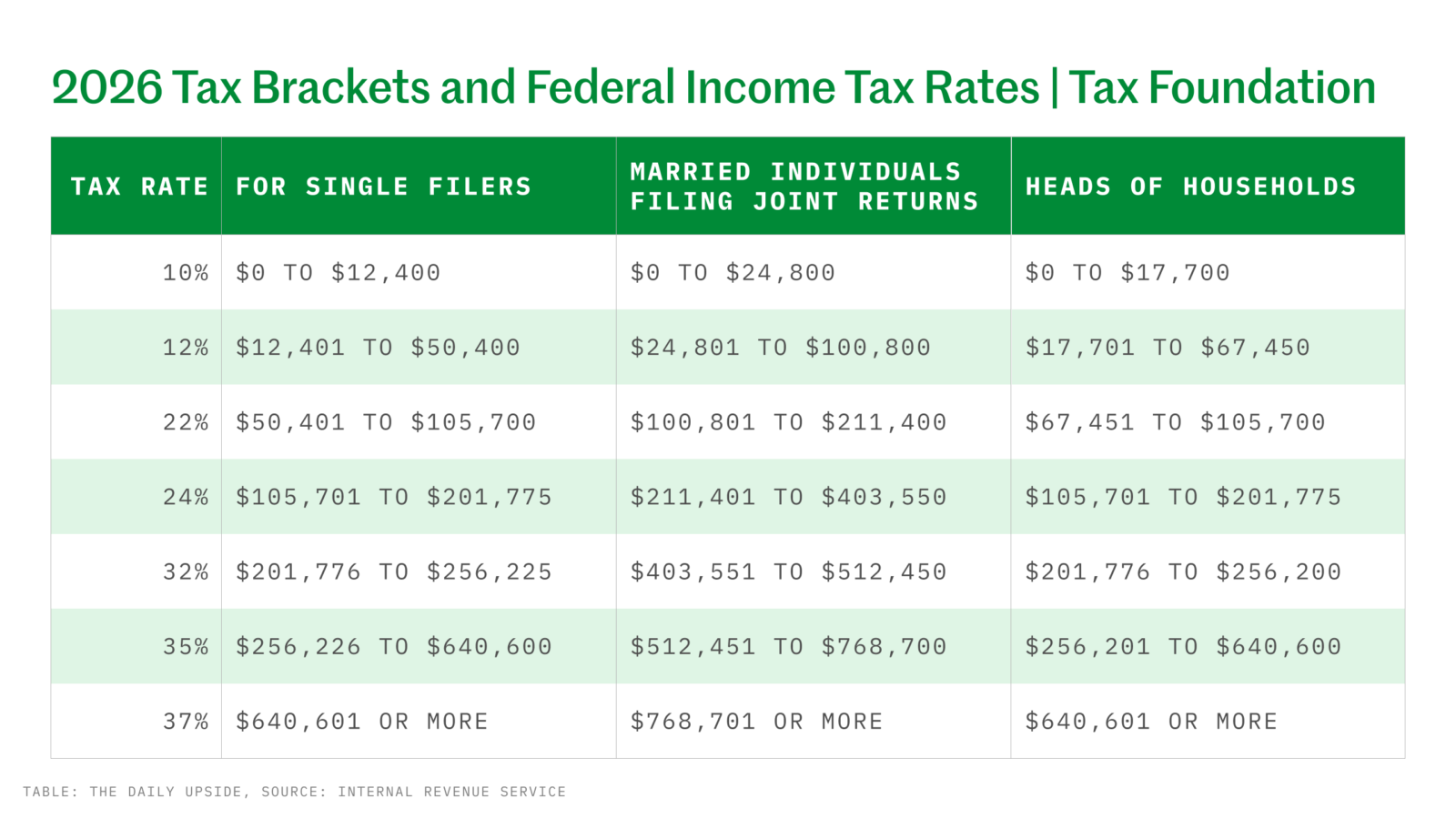

Manage to Marginal Tax Rates. Investment decisions have tax consequences. So, to the extent we can manage the tax brackets below, we add value. For example, we can manage how much of a Roth conversion the client should do. Or perhaps a retired client might be in the 0% federal long-term capital gains rate and can recognize gains with no federal taxes. (I typically recommend always using up the 10% and 12% marginal bracket and frequently using up all of the 24% bracket.) You can also assess how much benefit the client is getting from owning municipal bonds. And don’t forget state income taxes if the client is domiciled in a state that has income taxes.

Understanding Marginal Tax Rates on Capital Gains Is Also Critical. How much long-term gain can be recognized before the client hits the federal 20% marginal tax? Even if they are in the 15% marginal rate, are they being hit with the 3.8% net investment income tax (income over $200,000 single and $250,000 married filing jointly)? Often, the client can spread the gain over a couple of years.

Assess the Benefit of Debt. I’ve noted for decades that a mortgage is the inverse of a bond. If the client has enough liquidity, it rarely makes sense to borrow money at a higher after-tax rate than they lend it out at. Look at the clients’ itemized deductions in schedule A and compare the after-tax cost of the debt to the after-tax interest income they are receiving on a high-quality bond in their taxable account. Paying off the debt is typically what I call “low hanging fruit” in that it provides a risk free and tax-advantaged higher return than bonds.

Make Charitable Contributions the Right Way

Don’t tell clients how much they should be donating to charity or which charities to donate to, but advise clients that they can do this in a tax-efficient way and still provide the same benefit to the charity. If you see they have made large cash contributions, explore making large lumpy donations of appreciated security to a low-cost Donor Advised Fund and doing so every few years rather than annually. The appreciated security can then be sold in the DAF without taxable consequences. Then, over the next several years, the client can have the fund give to that same charity.

This gives them both tax savings from avoiding taxes on those unrealized gains and a much bigger tax-benefit from the gift itself. And you get a bonus for the client if they have such an underperforming investment with a big gain.

If the client is over 70.5 years old, a qualified charitable distribution is even better. A QCD allows those individuals to donate up to $111,000 total to one or more charities directly from a taxable IRA instead of taking their required minimum distributions. This not only reduces taxable income, it reduces the client’s modified adjusted gross income, which helps with other taxes such as the Medicare premiums from the Income-Related Monthly Adjustment Amount.

Find Investment Deductions They Haven’t Been Taking. The biggest miss I see is that the client’s CPA typically hasn’t taken a state deduction from interest income from US government obligations (such as Treasury bills, notes and bonds). They are exempt for state and local income tax. Most (but not all states) allow a deduction from a fund that has some government interest. For example, the Vanguard Total Bond Market ETF (BND) had 44.06% of its income from US government obligations.

Another example of tax alpha is using a health savings account like a Roth. I often tell clients to max out their HSA contributions but pay for medical costs from taxable money. They can then keep the receipts and reimburse themselves tax-free decades later.

These are only some of the insights one can gain from a tax return. Remember, finding that tax-alpha can actually be better than trying to beat the market.

Direct Indexing Superuser Secrets Revealed

Powered by personalization, ongoing tax benefits, and differentiated client experiences, direct indexing has become a business growth engine.

To uncover what drives success, Northern Trust Asset Management surveyed top advisors at high-AUM firms and interviewed DI Superusers to reveal the strategies producing real results.