Good morning.

It’s an IPO for the Age of Aquarius.

According to a Financial Times report, Elon Musk wants the public market debut of SpaceX to coincide with a rare planetary near-alignment of Jupiter and Venus. It’s what astrology types call a conjunction, and with those two planets, it’s believed to foster prosperity, joy, optimism and all-around good vibes. The conjunction also just so happens to align with Musk’s 55th birthday on June 28 (yes, that’d make him a Cancer; yes, we did have to Google that). And if you’re wondering why Jerome Powell and the Federal Reserve didn’t lower interest rates yesterday, you no doubt overlooked the fact that the moon was in the Seventh House.

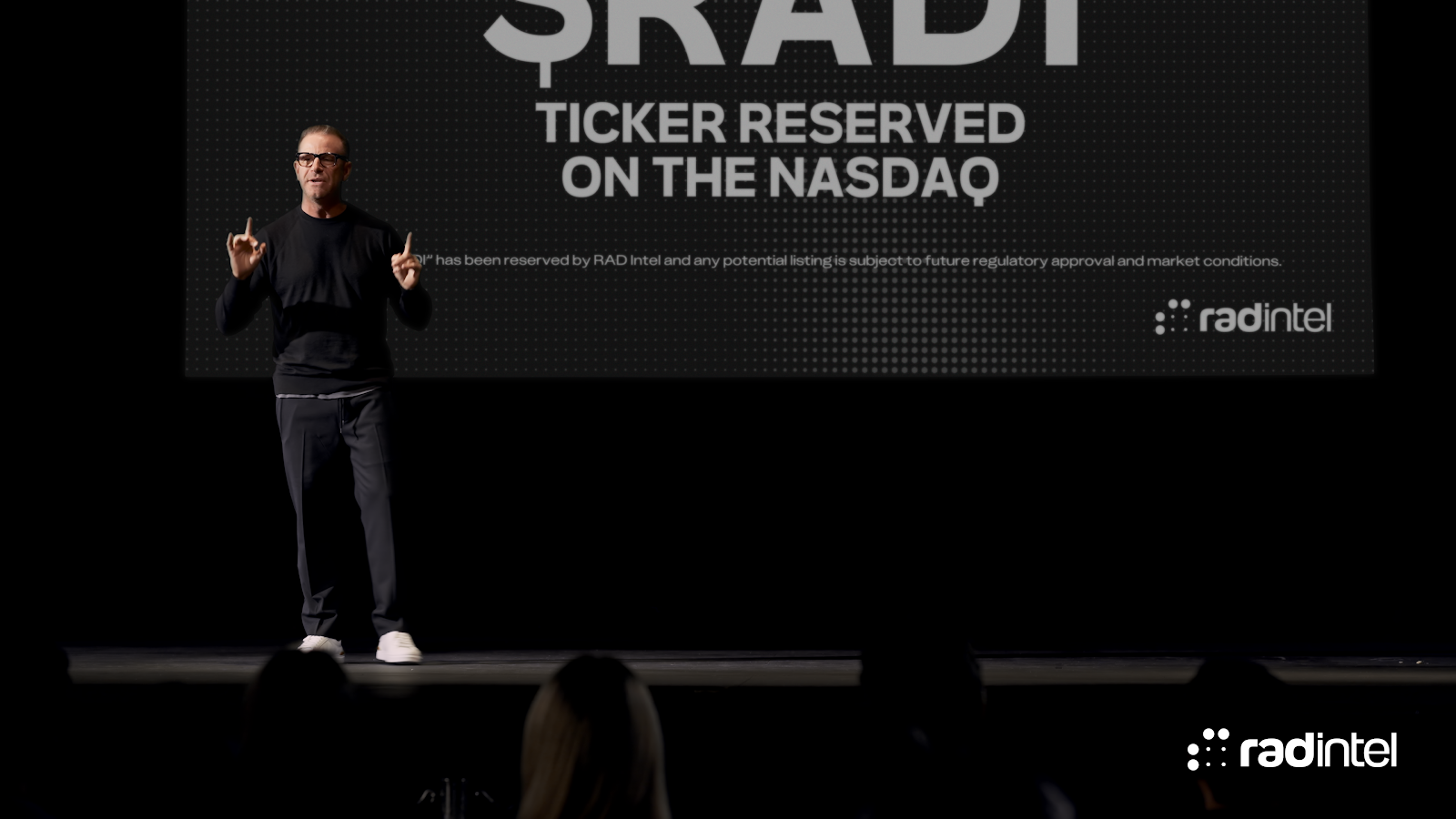

Nasdaq Ticker Secured: $RADI

Nasdaq ticker secured: $RADI. Still private. That’s a rare window. RAD Intel just locked $RADI as momentum keeps building. $60M+ raised from 14,000+ investors, backed by multiple Fidelity funds and selected by the Adobe Design Fund. Shares are still available at $0.85 in an SEC-qualified Reg A+ offering, subject to availability.

Tether Outbuys Most Central Banks in Gold Bunker Buildup

Tether, the company behind the largest stablecoin by market cap, is amassing a huge pile of gold bullion in a former Swiss nuclear bunker. The “James Bond kind of place,” as its CEO, Paolo Ardoino, described the storage facility to Bloomberg, houses a gold collection of more than 140 tons. With gold’s ongoing rally, that’s about $24 billion worth.

The crypto company bought at least 70 tons of gold last year, Bloomberg calculated, or more than was reported by any central bank besides Poland’s. Now, Ardoino said, it’s stockpiling two tons a week and plans to continue that pace at least through this quarter.

You’re So Golden

Tether’s main business is its eponymous stablecoin, also called USDT, which dominates the sector with more than $186 billion in circulation. Tether then invests the money it gets from folks buying USDT in other assets such as Treasuries and gold, profiting from the interest.

The company’s been piling up gold both for its own reserves and for its Tether Gold product, a token that’s growing as an alternative way for investors to gain exposure to the precious metal:

- Tether has issued about $2.7 billion worth of its gold-tied token, XAUT, and thinks its circulation could expand to $5 billion to $10 billion this year. That’s small compared with ETFs, but Tether’s CEO expects it to grow as foreign countries eventually launch their own version of tokenized gold that could compete with USD.

- Tokenized gold is meant to be redeemable for physical gold, meaning Tether should be stockpiling enough gold to at least match the amount of XAUT its customers own (no selling out like Costco). If that promise is kept, it makes the product distinctive from so-called “paper gold” like ETFs, where the institution doesn’t necessarily have investors’ gold stored in a Swiss bunker.

Feeling Existential: Tether seems to be prioritizing buying gold because its value isn’t tied to governments as tightly as fiat currencies are. That degree of separation appeals to the crypto industry and its anti-centralization ethos, as well as the CEO’s very Gen Z-esque sense that, as he told Bloomberg, “The world is going towards darkness.” However, depending too much on the commodity could become a problem when its No. 1 stablecoin’s promise is a 1:1 tie with the US dollar, not gold. Plus, mainstream competitors are coming for Tether’s stablecoin throne, with Fidelity yesterday announcing a token of its own.