ETF CORNER PRESENTED BY

How Does Your Investing Strategy Compare to Peers’? Read Our Exclusive Conversation with State Street’s Maxwell Gold.

It’s the start of a new year — the perfect time to evaluate your diet, fitness regime, and your financial playbook. One of the best ways to evaluate your financial strategy is to compare yourself to your peers.

State Street Investment Management just launched a report, hot off the press, with invaluable insights on the state of investor sentiment as we head into the new year. The report explores the money habits of 3,000 retail investors that you can use to benchmark your own financial mindset. We interviewed State Street’s Head of Direct Retail, Maxwell Gold, to discuss some of the most compelling findings from the report. Read on for the highlights of that conversation.

Q: What was the most surprising insight from this year’s survey, and what does it tell us about people’s long‑term money habits and attitudes going into 2026?

A: There are a lot of interesting nuances to the report, but the two I found most interesting surrounded the types of accounts that investors are using, and how artificial intelligence (AI) is shaping investment decisions.

- Takeaway 1: Retail investors are building strong financial foundations — but there’s still room to grow.

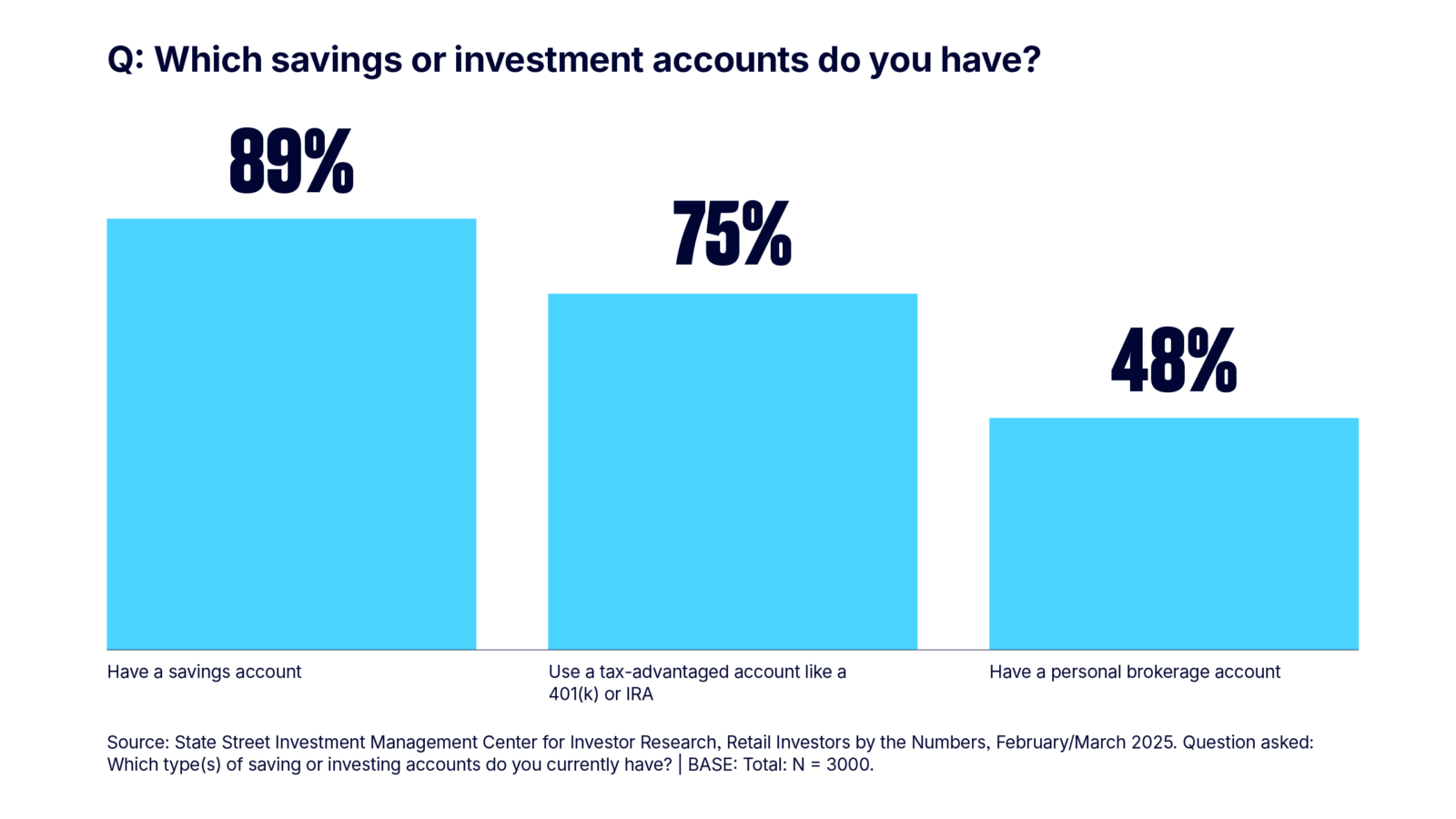

Our research shows that nearly 90% of retail investors have a savings account, and 75% are using tax-advantaged retirement accounts like a 401(k) or IRA.1 But when it comes to personal brokerage accounts, adoption drops off significantly: only 48% of investors currently use one.2

From my perspective, this is actually an encouraging signal. It suggests that many retail investors have built strong financial foundations and value financial security. But when we look at how investors allocate their monthly surplus income, a revealing pattern emerges.

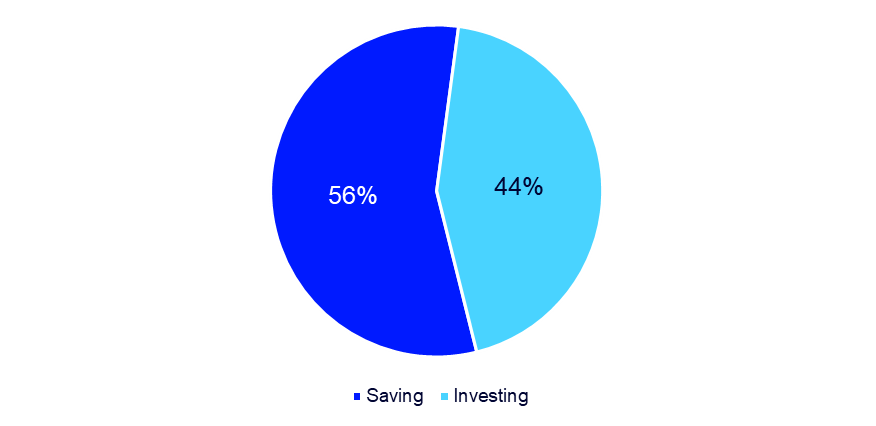

Our research shows that retail investors currently allocate 56% of surplus income to savings and 44% to investing.3 While savings remains critical — particularly for liquidity and peace of mind — this imbalance suggests that many investors may be staying conservative even after establishing core savings and retirement accounts.

For those investors, it raises an important question: are additional dollars positioned to support long-term growth? With the right educations and guidance, modest shifts toward investing can help investors participate more fully in market growth as their financial circumstances evolve.

- Takeaway 2: AI interest is growing, but adoption remains measured.

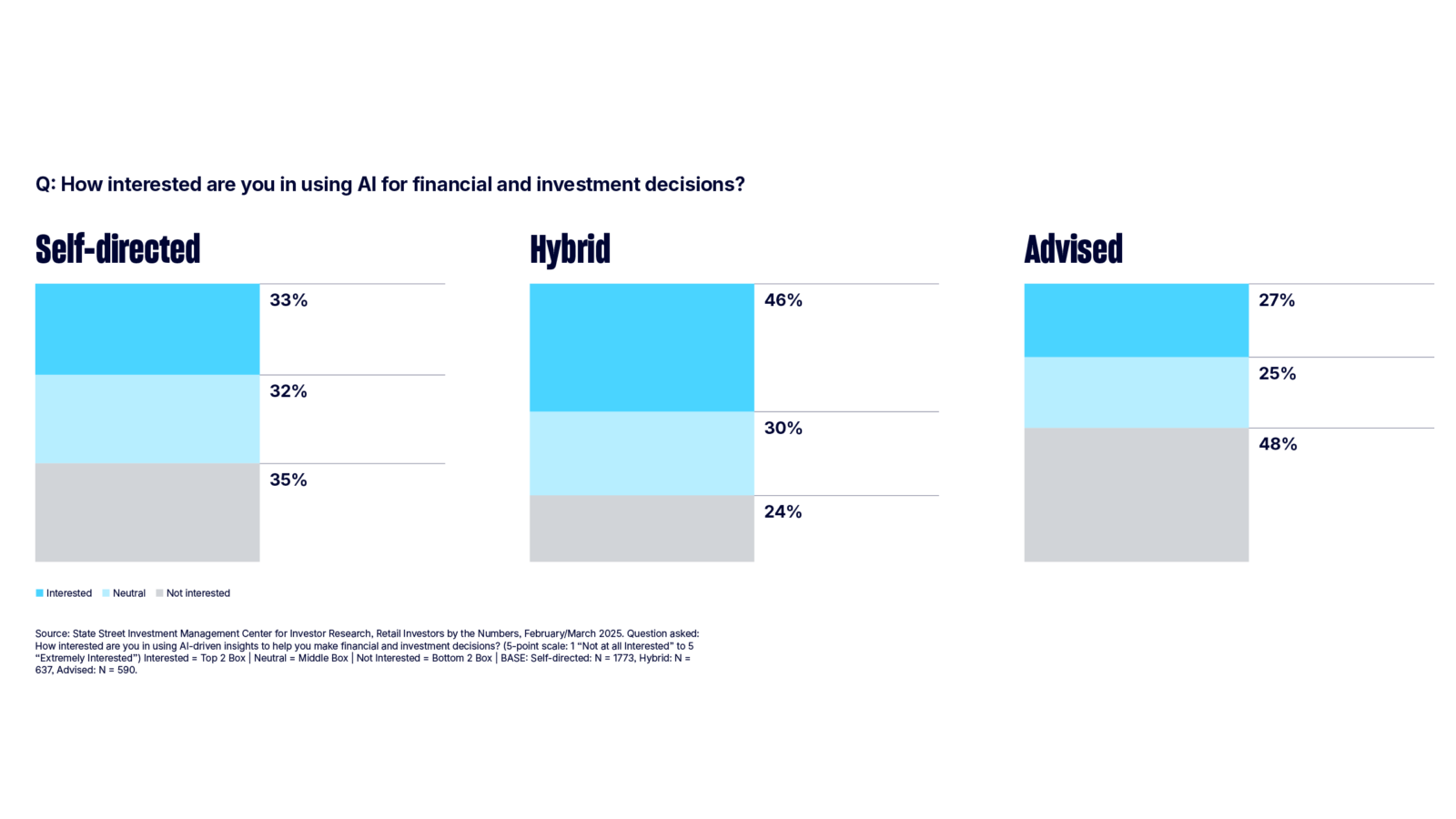

We also asked retail investors about their interest in using AI to support financial and investment decisions. Among self-directed investors, 33% expressed interest in using AI in this capacity.4

Given the level of attention AI received in 2025, and just how much adoption we’ve seen into many aspects of daily life, I would have expected that number to be slightly higher. This may suggest that investors are still taking a cautious approach when it comes to AI adoption into their financial lives. AI generated suggestions may be acceptable when working on an email, but it seems that same level of adoption and trust hasn’t permeated yet to important personal financial strategies and decisions for most individuals.

That said, I see this as a sign of where the industry is headed, not a limitation. We are in the very early innings of understanding AI’s capabilities and how it will impact the landscape, and there’s no question that adoption will increase across facets like investor education, market insights, and decision support. We’re not quite there yet, but it’s something we’re watching closely.

Q: How do investing attitudes and retirement approaches change across generations? Are there any differences you didn’t expect?

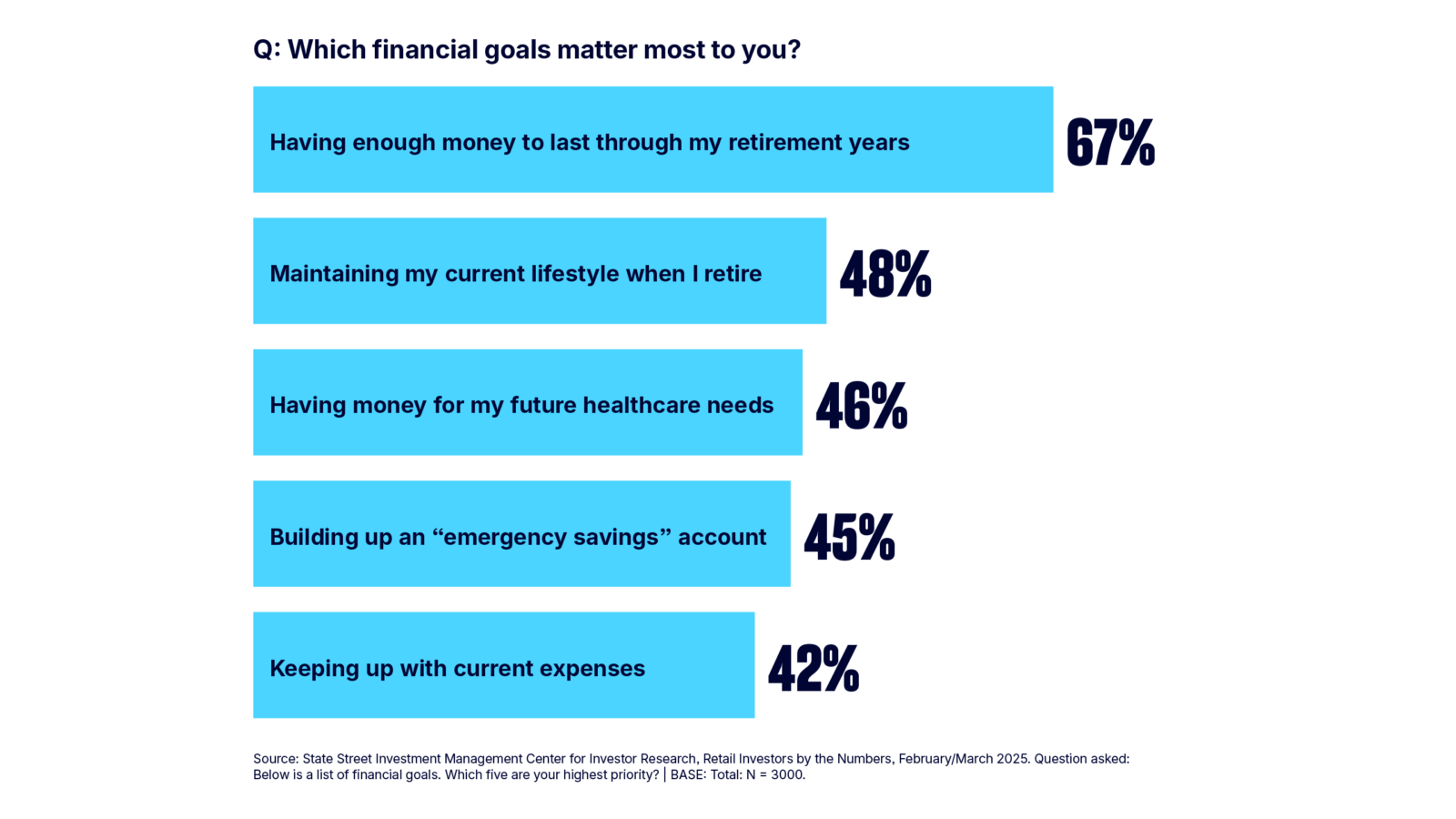

A: There’s a lot of coverage in the popular media about differences in how Gen Z and, let’s say, the Boomer generation, approach finance. And some of it is fair, the wealth continuum absolutely skews toward the older generation. But we’re fascinated to see just how much commonality surfaced in our findings. For example, retirement planning consistently emerges as one of the top financial priorities. 35% of Gen Zers, popularly portrayed as more concerned with TikTok than taxes, said that having enough money to last through retirement was one of their top financial priorities.

Overall, two-thirds of retail investors (67%) are concerned about having enough money to last through retirement, and nearly half (48%) say maintaining their current lifestyle in retirement is a primary goal.5 Those concerns are remarkably consistent across segments.

Today’s economic environment shows that macro concerns over things like inflation and affordability are pervasive. For us, it underscores even stronger the importances we need to place on education and building toward long-term goals.

Q: What pitfalls do emotions and behavioral biases present for retail investors, and how can they guard against them?

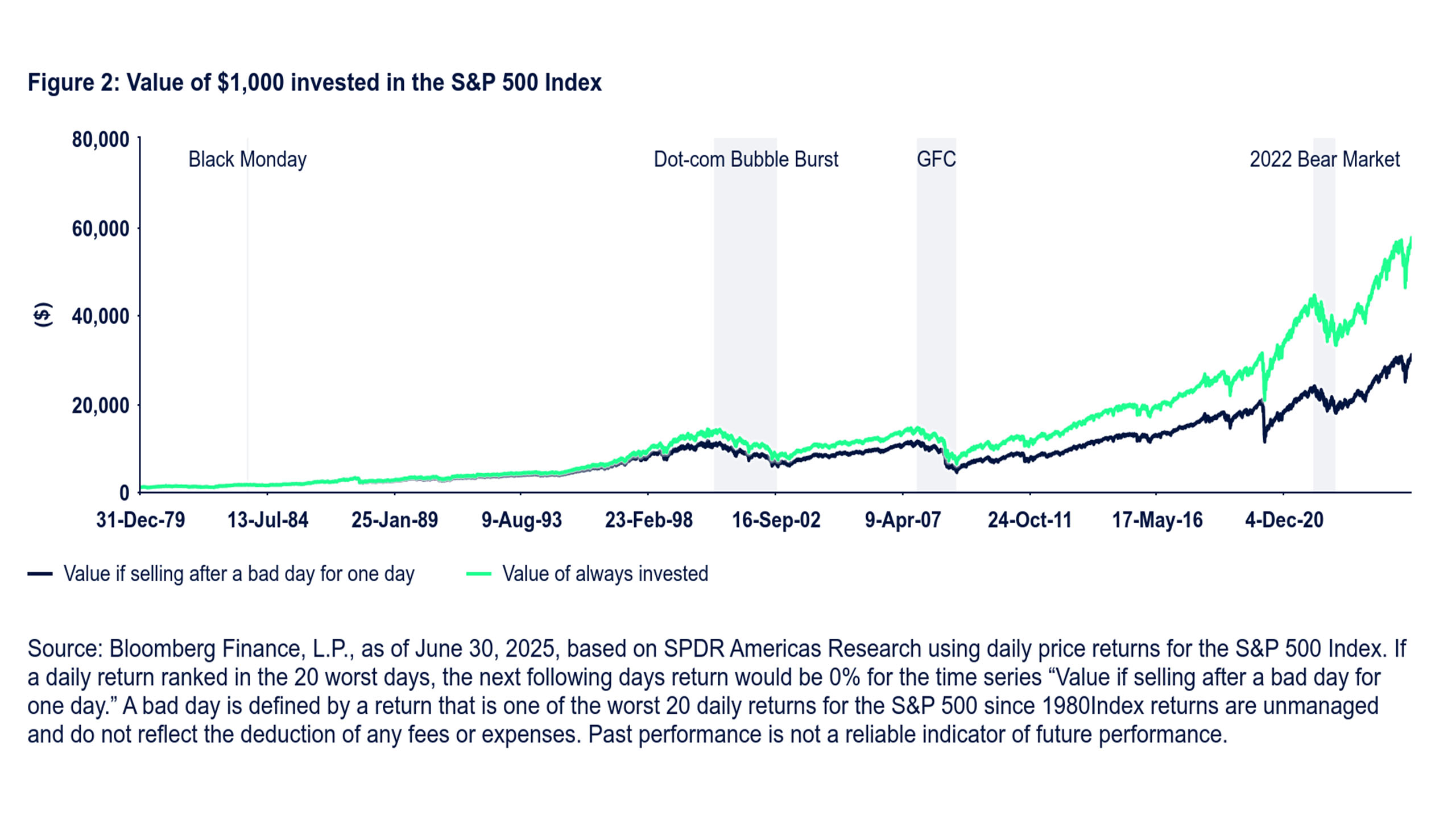

A: To me, one of the cornerstones to wealth building and financial independence has always been that long-term success is driven more by time in the market versus timing the market. In my view, individual investors who start early, invest consistently, and stick to a disciplined approach through market cycles, put themselves in a strong position to build wealth over time.

Timing the market can be costly.

Value of $1,000 invested in the S&P 500 in 1926, 1960-2024

In recent years, we’ve seen significant growth among younger generations, particularly Gen Z and millennials, who are starting to invest earlier as part of their path to financial security. That’s a very positive trend.

That said, our findings as previously highlighted also show that when retail investors have extra money left over each month, they’re still more likely to increase their savings than invest those dollars in the market.6 This tendency may reflect a natural risk-averse bias, which may be amplified by the current economic environment.

Q: What percentage of your monthly surplus income do you allocate to saving versus investing?

Source: State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: What percentage of your monthly surplus income (i.e., money not spent on expenses) do you typically allocate to saving versus investing? | BASE: Total: N = 3000

A: The challenge — and opportunity — for retail investors is to avoid letting short-term emotions override long-term objectives. Investors who maintain a long-term perspective and recognize that the potential long-term benefits of investing often outweigh short-term volatility are better positioned to navigate market cycles and stay aligned with their financial goals.

Q: Against a backdrop of shifting investor psychology, why do ETFs remain attractive for many, and should investors think about them differently than individual‑stock portfolios?

A: ETFs have been a powerful tool for retail investors ever since the first US-listed ETF, S&P 500® ETF Trust (SPY), was launched 30+ years ago. And with the launch of other broad-market ETFs like the SPDR® Dow Jones® Industrial Average℠ ETF Trust (DIA) , ETFs helped democratize investing by providing cost-efficient, liquid access to broad-market indices, such as the S&P 500 Index and the Dow Jones Industrial AverageSM.

Today, ETFs go well beyond simple index tracking. They serve as flexible building blocks that allow all investor types to access global markets and asset classes (like emerging markets, fixed income, credit, commodities, etc.). And they can provide exposure to thematic, sector, or actively-managed investing strategies — all within a single, easy-to-use wrapper.

One of the most standout benefits of ETFs is their diversification. By holding a basket of securities rather than a single stock, ETFs can help take the guesswork out of picking individual stock winners, reduce company-specific risk, and potentially simplify portfolio construction, which can be especially appealing during periods of market uncertainty. ETFs also trade intraday, just like publicly listed stocks, and are easy to trade on brokerage platforms.

Q: Which types of ETFs — broad‑market, income-focused, fixed income, sector, or niche — seem to resonate most with retail investors these days?

A: Retail investors continue to show strong interest across a range of ETF categories, but income-oriented strategies, thematic ETFs, and broad-based equity funds remain particularly popular. These exposures align well with investors’ dual goals of generating income and maintaining diversified, long-term market participation.

Precious metals, particularly gold, have especially stood out in terms of investor activity and flows — and retail investors are a major part of that. As gold prices reached new all-time highs in 2025 amid elevated global uncertainty, gold ETFs saw a corresponding rise in assets and investor interest.

The investment case for gold has gained renewed attention among retail investors in the US and around the globe. Factors such as central bank purchases, consumer and jewelry demand, and a conducive macroeconomic backdrop have all contributed to this trend moving into 2026.

Q: What should advisors and individual investors keep top of mind when using ETFs to balance liquidity, return potential, and risk management? As retail sentiment evolves and markets face uncertainty, how do ETFs offer a uniquely flexible, diversified option for thoughtful investors?

A: In all markets, it’s important for investors to stay focused on their long-term investment objectives. And in my opinion, ETFs are a fantastic tool that allow you to do that: they’re flexible portfolio building blocks that offer access to a wide range of strategies, all within a single, efficient structure. And they can serve many roles in a portfolio — from capital appreciation and growth, to risk management, to income generation.

That flexibility still requires discipline. ETFs are most effective when used within a clear asset allocation and rebalancing approach to help manage portfolio risk over time. As markets continue to rally and assets reach new highs, investors should periodically review their asset allocation positioning (individually or with a financial advisor) to ensure market-driven drift hasn’t steered them away from their intended investing strategy.

There’s been a tremendous number of retail investors entering the market ever since the COVID-19 pandemic. And because many are younger and newer to investing, they often have not experienced a sustained bear market with a lengthy recovery period — like the Great Financial Crisis (2008), Dot-Com Bubble (2000), or Black Monday (1987).

That’s why it’s so important for retail investors to consider broad diversification across asset classes and market environments. Used thoughtfully, ETFs provide an accessible way to stay diversified, manage liquidity, and remain invested through market cycles without losing sight of long-term goals.

For additional resources, visit State Street Investment Management to learn more about ETF investing and to access the full retail investor report.

Footnotes

1State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: Which type(s) of saving or investing accounts do you currently have? | BASE: Total: N = 3000.

2State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: Which type(s) of saving or investing accounts do you currently have? | BASE: Total: N = 3000. State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025.

3Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: What percentage of your monthly surplus income (i.e., money not spent on expenses) do you typically allocate to saving versus investing? | BASE: Total: N = 3000.

4State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: How interested are you in using AI-driven insights to help you make financial and investment decisions? (5-point scale: 1 “Not at all Interested” to 5 “Extremely Interested”) Interested = Top 2 Box | Neutral = Middle Box | Not Interested = Bottom 2 Box | BASE: Self-directed: N = 1773, Hybrid: N = 637, Advised: N = 590.

5State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: Below is a list of financial goals. Which five are your highest priority? | BASE: Total: N = 3000.

6State Street Investment Management Center for Investor Research, Retail Investors by the Numbers, February/March 2025. Question asked: What percentage of your monthly surplus income (i.e., money not spent on expenses) do you typically allocate to saving versus investing? | BASE: Total: N = 3000.

Important Risk Information

Investing involves risk including the risk of loss of principal.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs net asset value. Brokerage commissions and ETF expenses will reduce returns.

Diversification does not assure a profit or protect against loss in a declining market.

Distributor: State Street Global Advisors Funds Distributors, LLC, member FINRA, SIPC, an indirect wholly owned subsidiary of State Street Corporation. References to State Street may include State Street Corporation and its affiliates. Certain State Street affiliates provide services and receive fees from the SPDR ETFs. ALPS Distributors, Inc., member FINRA, is the distributor for DIA, MDY and SPY, all unit investment trusts. ALPS Portfolio Solutions Distributor, Inc., member FINRA, is the distributor for Select Sector SPDRs. ALPS Distributors, Inc. and ALPS Portfolio Solutions Distributor, Inc. are not affiliated with State Street Global Advisors Funds Distributors, LLC.

Before investing, consider the funds’ investment objectives, risks, charges and expenses. To obtain a prospectus or summary prospectus which contains this and other information, call 866.787.2257 or visit ssga.com. Read it carefully.

Expiration 01/31/27

Not FDIC Insured * No Bank Guarantee * May Lose Value

Adtrax: 8690968.1.2.AM.RTL SPD004394

Recent News

-

For Elderly Clients, Home Design Is the New Hot Ticket

Photo via Eduardo Barraza/ZUMAPRESS/Newscom -

Anthropic Bets Big on Wealth Management with New AI Tools

Photo via VCG/Newscom -

Ritholtz Wealth Files for First ETF

Photo via Connor Lin / The Daily Upside -

Who Will End Up Paying for Nvidia’s Boom?

Photo via Lance Jording/ZUMAPRESS/Newscom -

US Housing Market Doesn’t Have Much ‘Tailwind’: Lowe’s CEO

Photo by https://unsplash.com/photos/condo-neighborhood-in-the-suburbs-ROVuTYG_jso via Unsplash -

Salesforce Earnings Highlight Critical Choices Facing Legacy Software Firms

Photo via Andrew Schwartz/SIPA/Newscom -

Advisors Lean on Legacy Planning to Help Secure Next-Gen Clients

Photo by Getty Images via Unsplash -

What’s Driving Bitcoin’s Slump?

Photo by General Bytes via Unsplash -

Leverage Is Almost Everything for These ETF Issuers

Photo by Getty Images via Unsplash -

Home Depot Powers Past Housing Market Struggles to Notch Earnings Win

Photo by Oxana Melis via Unsplash