Good morning.

That service creep is getting real.

Planning services like budgeting, cash flow and tax preparation are baseline expectations for financial advisors, and now new research suggests you can add estate planning to that list, too.

Nearly 70% of advised clients said they would consider switching to an advisor who provides estate planning, according to a report from Trust & Will, a software company that provides those services. Interest was strongest among younger clients, who are expecting ongoing services, with advisors proactively identifying outdated or incomplete documents and recommending updates.

At this rate, clients might soon be asking advisors to help put together their IKEA furniture.

SpaceX Rocketing into Nasdaq-100 Spurs Questions from Clients

Houston, we have another mega-cap.

SpaceX going public on the Nasdaq was a momentous occasion as it became the largest offering in history, raising roughly $75 billion in its first day. And starting today, the Elon Musk-led rocket and artificial intelligence business will be added to the Nasdaq-100, meaning every client who holds funds tied to the index now has exposure to one of the biggest companies riding the one of the biggest hype trains ever. However, despite being one of the largest companies by market cap, SpaceX won’t be among the heaviest-weighted names in the index, The Wall Street Journal reported: Only 5% of its shares were sold during the IPO. The company is expected to have an index weight of less than 1%, based on Nasdaq-100’s float-adjusted methodology.

While the SpaceX weighting is small, for now, it’s something for advisors to monitor as clients continue asking questions about getting exposure to a company that landed the largest initial public offering in history.

Ground Control to Major Tom

There are plenty of ways to give clients exposure to the Nasdaq and ultimately SpaceX, with the Invesco QQQ Trust (QQQ) and the Invesco NASDAQ 100 ETF (QQQM) being the most popular choices. The two funds manage roughly $600 billion in assets combined. However, other issuers are looking to undercut Invesco and provide stiff competition:

- The two Invesco ETFs have fees of 18 and 15 basis points, respectively.

- State Street’s new SPDR Portfolio Nasdaq100 fund (QNDX) is charging just 10 bps.

- Meanwhile, BlackRock’s upcoming iShares Nasdaq 100 ETF (IQQ) is expected to target a management fee of around 12 basis points.

Other funds with exposure to the Nasdaq include the Fidelity Nasdaq Composite ETF (ONEQ), the JPMorgan Nasdaq Equity Premium Income ETF (JEPQ) and the First Trust Nasdaq-100 Select Equal Weight ETF (QQEW).

Sitting in a Tin Can. While all of this is exciting news for SpaceX and asset managers, it may not have the biggest impact inside client portfolios. “SpaceX joining the Nasdaq-100 certainly raises questions among clients,” said Nathan Mueller, founder of BlackBird Finance. “However, it isn’t something that will warrant changes to the portfolio,” he said, adding that a long-term investment plan has to consider bonds, alternatives, international securities and plenty of US equities, most of which are found outside of the Nasdaq. “[The index] starts to feel like a smaller, less significant piece of their overall portfolio.”

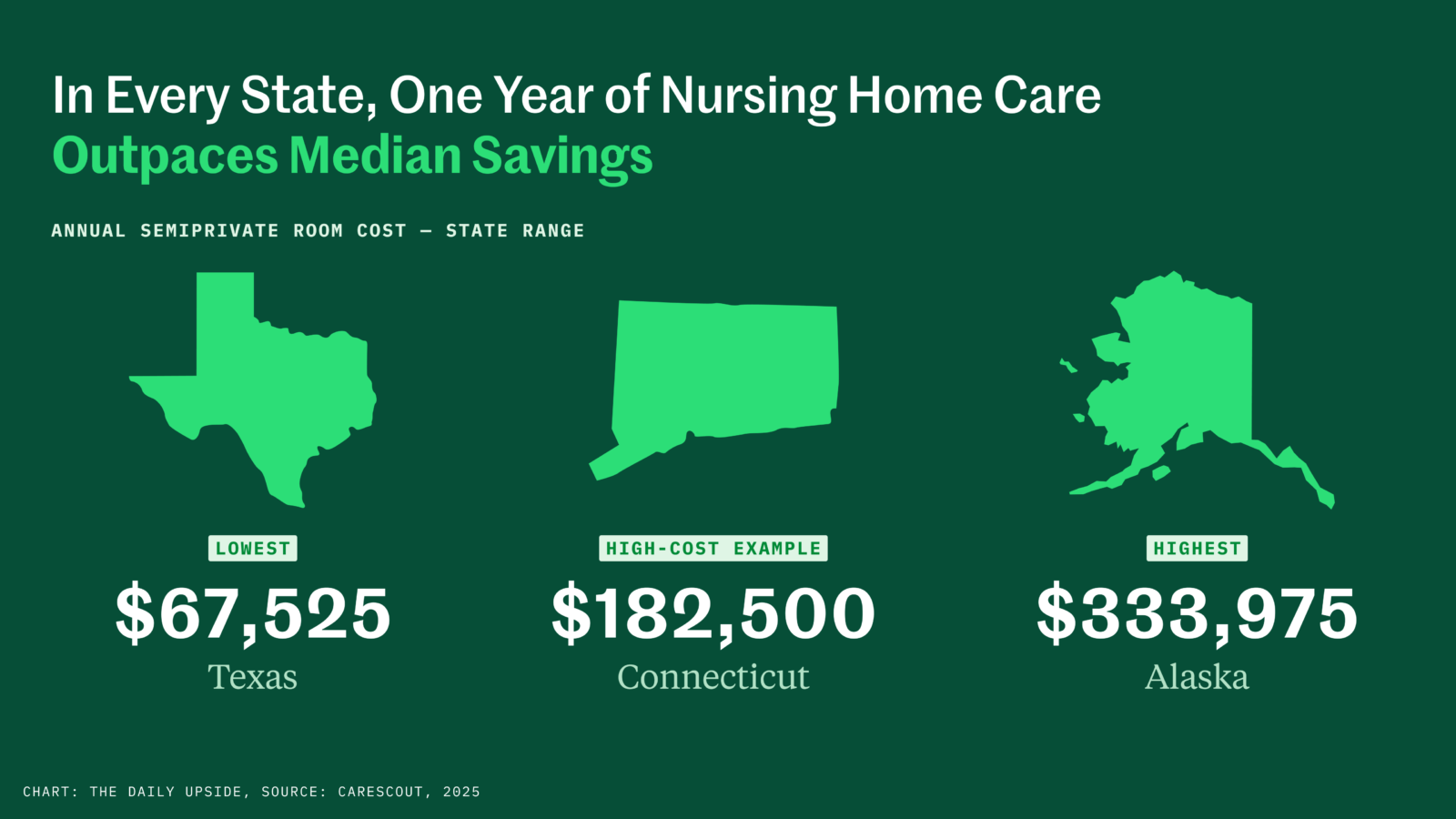

Even Big Portfolios Can Buckle Under Care Costs

Some of your wealthiest clients may assume they can self-fund their long-term care. But even significant savings can be outpaced by the costs, which are front-loaded, unpredictable, and inflationary. MassMutual Wealth Management’s Michael Leanch has an approach that can help you plan their LTC coverage before the costs hit. Read more.

IRS Eases Gift Tax Rules for Trump Accounts

Gift tax returns? We don’t need no stinkin’ gift tax returns.

The IRS released new guidance last week that largely (but not entirely) resolves concerns about Trump account contributions inadvertently triggering burdensome gift tax reporting requirements for families and individuals. Revenue Procedure 2026-25 provides what is essentially a transfer tax waiver that treats Trump account contributions as completed “current interest” gifts rather than “future interest” gifts when those contributions meet certain requirements, preventing the need to pay and report gift taxes. That may sound like a technical nuance, according to Kevin Matz, partner at ArentFox Schiff, but the practical implications are significant for taxpayers and the IRS.

“The IRS received about 300,000 Form 709 gift tax returns in fiscal 2025,” Matz told Advisor Upside. “In contrast, because nearly 6 million elections to open Trump accounts have already been received, the number of gift tax returns filed annually could have exploded to several million.” That’s off the table now, Matz said, but the IRS guidance is not a blanket policy for all Trump account contributions, so advisors and their clients need to study up on the rules to ensure compliance.

Not Any Old Gift

Trump account contributions are technically structured as taxable gifts. Put simply, that’s because the funds are inaccessible to the child until age 18. That technically makes the contributions “future interest” gifts under the tax code, which normally triggers taxation and must be reported on a Form 709 gift tax return. Statutory language notwithstanding, Matz said, it was not Congress’ intent to make Trump account contributions taxable future interest gifts that can’t be counted as part of a taxpayer’s annual gift tax exclusion, set at $19,000 per recipient in 2026. Hence Revenue Procedure 2026-25 and its gift tax waiver or “safe harbor.”

“It’s undeniably helpful for taxpayers who fit within the scope of the revenue procedure, because it is complex and expensive to prepare Form 709,” Matz said. “However, the policy unfortunately creates two different treatments of Trump account contributions, depending on what situation the taxpayer is in.”

The safe harbor requirements (simplified) are as follows:

- The taxpayer is an individual whose only would-be taxable gifts during the year are cash contributions to one or more Trump accounts that do not exceed the annual exclusion amount.

- Their contributions to Trump accounts don’t generate either a gift or generation-skipping transfer tax liability, after application of the taxpayer’s remaining applicable credit amount against the gift tax or remaining GST tax exemption.

- Disregarding the Trump account contributions described above, no gift tax return is otherwise required to be filed for other purposes.

A Permanent Fix? Presumably, the Treasury and the IRS didn’t believe that they possessed the authority to grant broader, across-the-board relief based on the statutory language Congress adopted, Matz said. He believes Congress should therefore consider a technical correction to the statute to eliminate the disparate treatment of Trump account contributions.