Most clients plan to live into their 80s or 90s. It’s a blessing brought by advances in healthcare and longevity science. But with that blessing comes a significant expense that far too few people plan for: the soaring cost of long-term care.

Michael Leanch, head of business development in MassMutual’s wealth management business, shares the framework he recommends for deciding who pays and in what order, why even substantial wealth often isn’t enough to cover costs, and how to build a plan before a crisis ever forces the question.

The LTC Triangle

A decisive question in long-term care planning is who pays, and in what order. Leanch structures that decision around what he calls the “LTC Triangle,” a clear sequence of funding sources that gives advisors a repeatable way to frame the conversation.

Individual resources come first, meaning the client’s own insurance and dedicated reserves. This is the layer that buys the most control and the widest choice of care, and it is where a thoughtful plan does most of its work. Family support sits second, a flexible but deliberately bounded layer, with clear limits set in advance so that care preserves family relationships rather than strains them. Government assistance ranks last, the safety net of last resort, and not, Leanch stresses, the plan itself.

From there, he urges advisors to stress-test the plan both quantitatively and qualitatively: project costs with real inflation, model self-funded versus insured scenarios, quantify the family’s actual capacity in time and money, and map out Medicaid triggers where relevant. “The goal of every advisor,” he said, “should be to maximize optionality for clients while minimizing unintended transfers of burden.”

Key Considerations

That order is clean on paper. In practice, two assumptions tend to distort it, and a sound plan tests both.

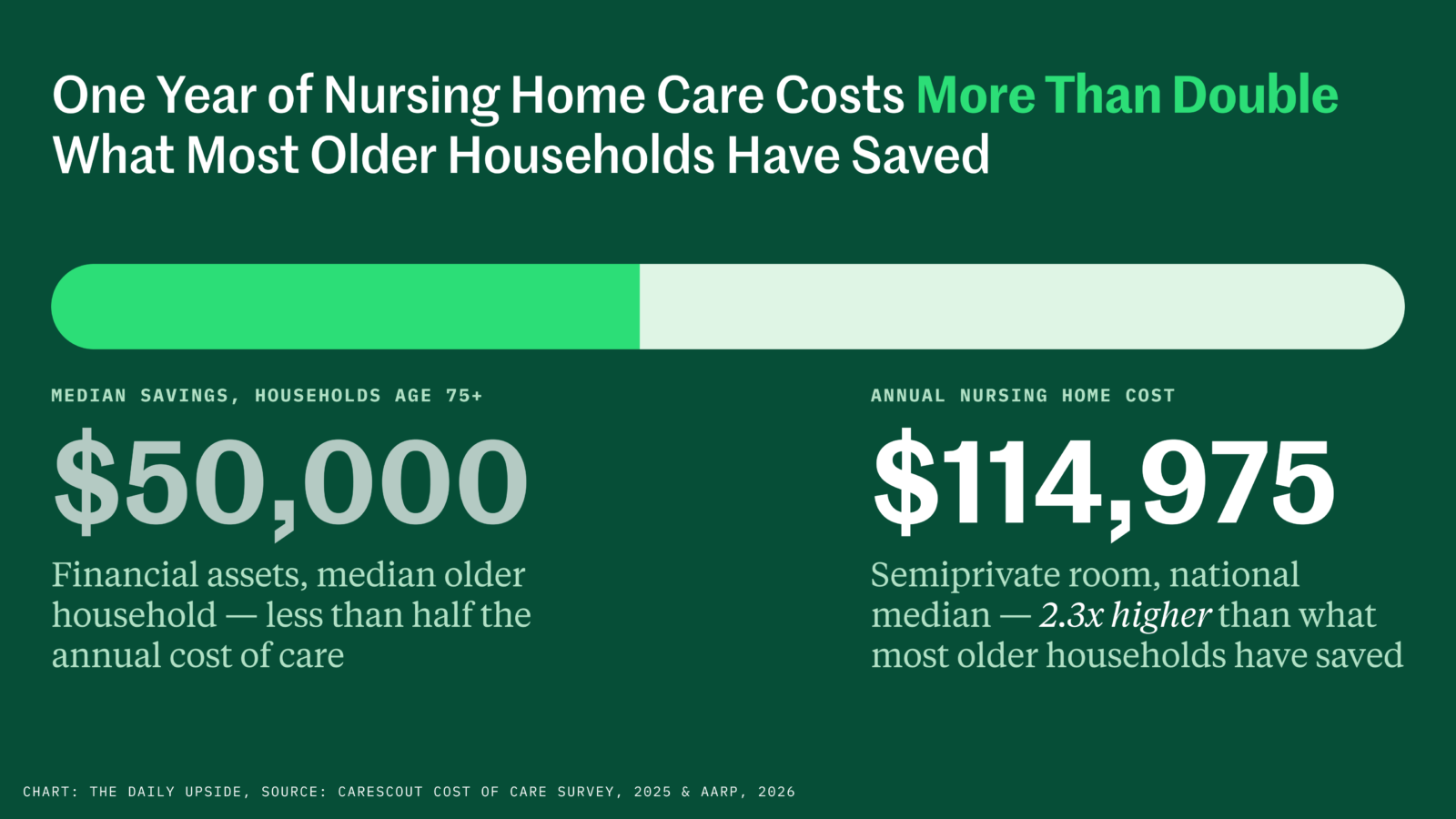

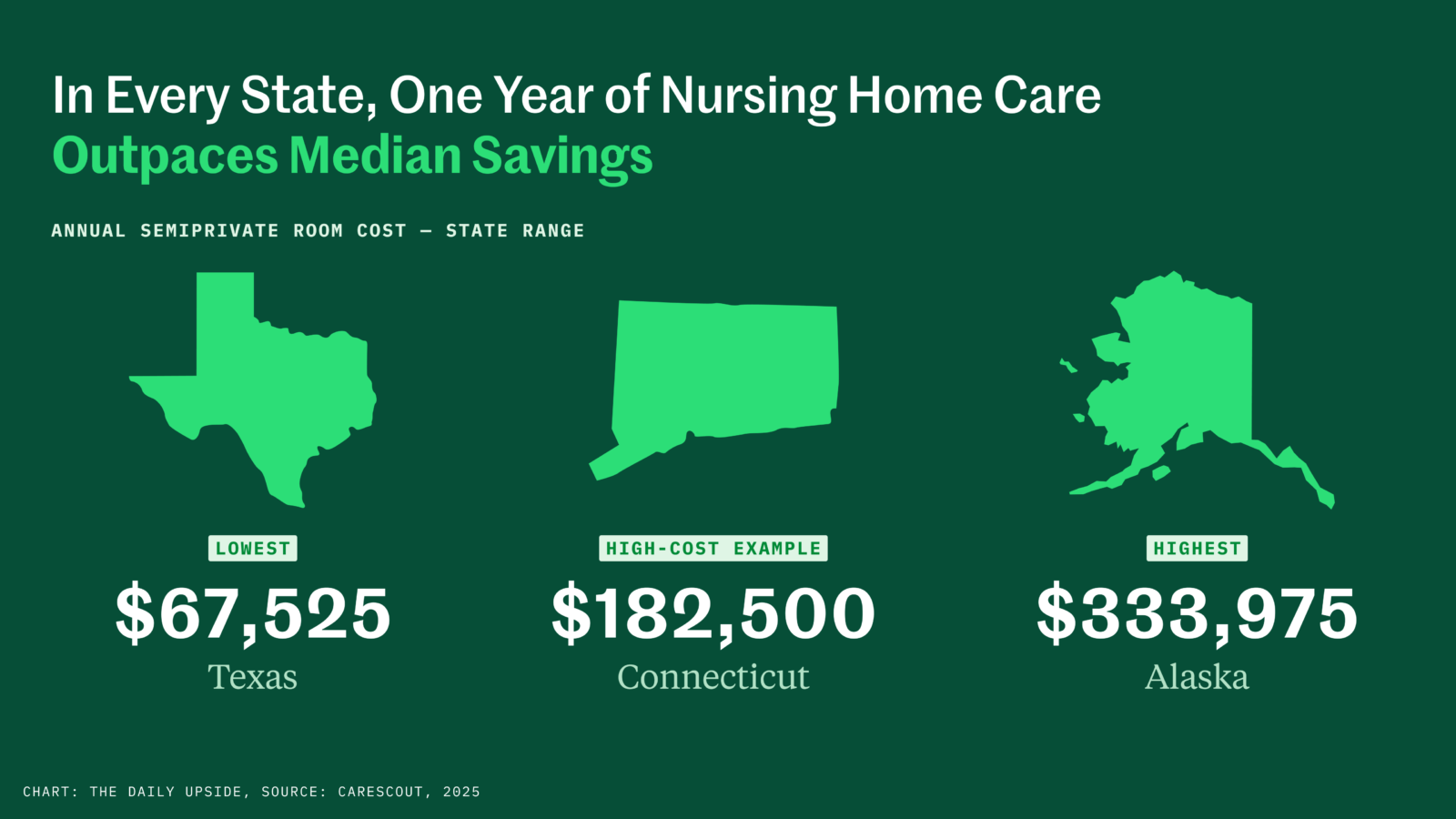

The first is the most common among affluent clients: that they can simply self-fund. Leanch concedes the logic holds, but only for a narrow group: ultra-high-net-worth families with liquidity buffers exceeding roughly $1 million per person, strong investment returns, and disciplined spending can absorb the volatility without much impact. For most, however, the math breaks down. Long-term care costs are front-loaded, unpredictable in duration, and inflationary. Self-funding exposes a portfolio to sequence-of-returns risk, crowds out other goals, and transfers financial risk to the family. Long-term care insurance, by contrast, may help transfer some of that cost away from the client’s balance sheet, depending on the structure and coverage selected.

That calculus helps explain why hybrid policies, linked life or annuity contracts with an LTC benefit, have gained significant market share relative to standalone coverage. Hybrids solve the “use it or lose it” fear by providing a death benefit if care is never needed, with premiums that are often guaranteed or paid in a limited window. The appeal can be meaningful for some clients. Leanch cautions that hybrids may be less efficient, and in some cases may not scale as well for very high or prolonged care needs. His advice is for advisors to pressure-test both options across multiple scenarios, instead of accepting the no-lose pitch at face value.

The second assumption is equally dangerous, because it feels like a backstop: that Medicaid will be there as a real safety net. In reality, Leanch said, Medicaid is a payer of last resort with strict eligibility. Clients must spend down countable assets to very low limits, after a multiyear look-back period on asset transfers. A home and one car are often exempt (though this varies by state) but most savings, investments, and second properties are counted. Even once a client qualifies, care may be limited to available Medicaid beds and providers, often with waitlists. Spousal protections exist but aren’t unlimited. “It protects basics,” Leanch said, “but rarely preserves dignity, choice, or legacy.”

The Cost of Getting It Wrong

The cost of getting long-term care planning wrong extends far beyond the balance sheet. “In my experience, the damage often hits relationships first, before the portfolio depletes,” Leanch said. Unpaid family caregiving can lead to burnout, lost wages, and career pauses, particularly for the so-called sandwich generation simultaneously supporting aging parents and their own children. Decision fatigue and conflict over care choices can erode family bonds quickly.

On the parents’ side, it accelerates the erosion of wealth that was meant to be passed down. On the children’s side, it can delay major milestones or force abrupt lifestyle changes as resources are redirected toward care. Well-funded retirements can be hollowed out by just a few years of intensive care, leaving survivors financially exposed in ways no one anticipated, and legacies eliminated.

“The human costs, strained marriages and stressed-out adult children, frequently precede the balance sheet erosion.”

— Michael Leanch, MassMutual

The most expensive mistake of all is simply waiting. For clients in their 40s and 50s, the notion of needing long-term care can still seem a long way off, but delay can be costly. The mechanics get harder with age: securing coverage or adjusting a plan in one’s 70s or later often means materially higher premiums, reduced benefits, or outright denial on health grounds. “By waiting to have these conversations,” Leanch said, “it can cost clients flexibility and choice later in life.”

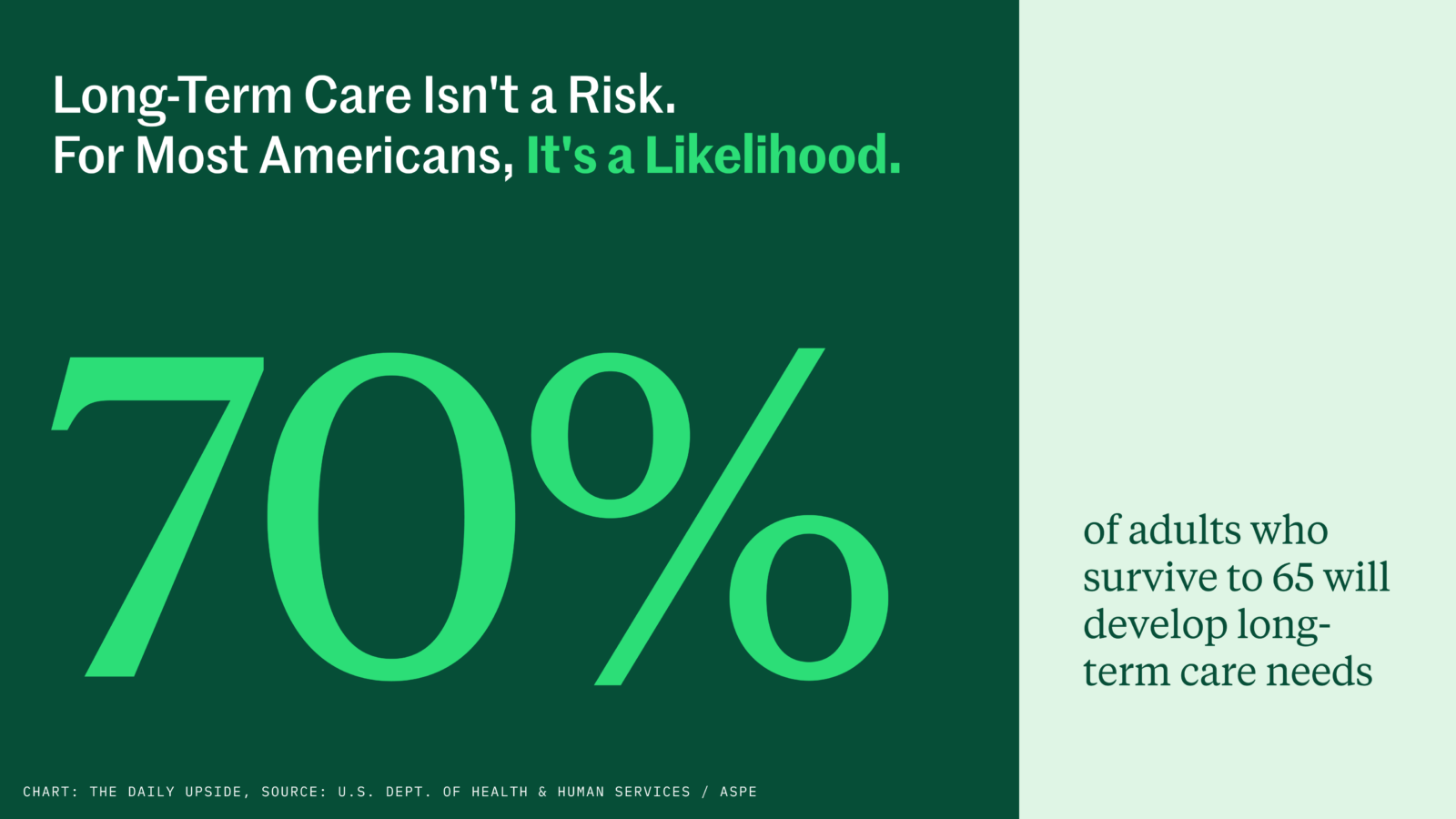

It is worth remembering the scale of the risk. Statistics show that 70% of people turning 65 may need some form of long-term care, yet 1 in 3 haven’t even considered how they’ll pay for it.¹ That stat applies to tens of millions of Americans, and likely more than a few on any advisor’s roster. Part of it comes down to an inherent optimism: no actuarial table can fully prepare someone for the prospect of losing mobility or facing cognitive decline. It is precisely that gap an advisor is positioned to close.

Where to Start

Closing that gap comes down to a sequence advisors can begin now. When clients ask what they can do to make sure the means are there when care is needed, Leanch points to a concrete, time-sensitive checklist:

- Model costs now, so the size of the risk is on the table before any decisions are made.

- Shop coverage in the 50s or early 60s, comparing traditional and hybrid options while rates and health still work in the client’s favor, and prioritize inflation protection.

- Build dedicated reserves earmarked specifically for these expenses.

- Coordinate the legal scaffolding: powers of attorney, trusts, and care directives.

- Bring the family into the conversation early, before a crisis forces it.

Handled this way, the plan can work on both sides of the ledger. Financially, it can help preserve portfolio longevity, sustain income, and protect a legacy. Just as importantly, it can reduce stress, widen the choice of care, and ease the strain on the family. Early action, Leanch said, can compound meaningfully, both financially and emotionally. “These conversations are some of the most valuable we facilitate in wealth management.”

¹ What Is the Lifetime Risk of Needing and Receiving Long-Term Services and Supports?, ASPE, 2019.

Insurance products issued by Massachusetts Mutual Life Insurance Company (MassMutual) and its subsidiaries, C.M. Life Insurance Company (C. M. Life) and MML Bay State Life Insurance Company (MML Bay State), Springfield, MA 01111-0001. C.M. Life and MML Bay State are non-admitted in New York.

Securities and investment advisory services offered through qualified representatives of MML Investors Services, LLC. Member SIPC and a MassMutual subsidiary. 1295 State Street, Springfield, MA 01111-0001.

Recent News

-

What’s the Magic Retirement Number? Check Your Clients’ ZIP Code

Photo by Nico Smit via Unsplash -

The Medicare Myths Costing Retirees Thousands

Photo by Getty Images via Unsplash -

Slowing Costco Sales Growth Unnerves Investors

Photo via imageBROKER/Iuliia Dombrovskaia/Newscom -

AstraZeneca Plunges After New Heart Disease Drug Fails Trial

Photo via IMAGO/CFOTO/Newscom -

Can SK Hynix Escape Chipmaking’s Cyclical Curse After Nasdaq Debut?

Photo via Yonhap News/YNA/Newscom -

Trump Accounts May Create Millionaire Gen-Beta Retirees

Photo by Curated Lifestyle via Unsplash -

BlackRock Takes On Invesco, State Street With New Nasdaq-100 ETF

Photo by David Tran via iStock -

Should Advised Clients Automatically Become Accredited Investors?

Photo by Getty Images via Unsplash -

Investors Find a Fashion Faux-Pas in Levi’s Upbeat Earnings

Photo via Xavi Lopez/ZUMA Press/Newscom -

Delta Introduces Business Class on a Budget

Photo via Nicolas Economou/ZUMAPRESS/Newscom