Good morning.

Ready to hit that fresh pow?

When someone gets caught running a Ponzi scheme, investigators often uncover some wild spending. But this one may take the cake. A Wisconsin man who operated as an unregistered financial advisor recently pleaded guilty to fraud and money laundering after defrauding nearly 200 investors out of more than $14 million. And what did he do with some of the money? Buy more than 300 snowmobiles.

One snowmobile makes sense. Two, if you want company. But 300 sounds more like the fleet you’d expect at a villain’s secret mountain lair, ready to deploy the moment James Bond arrives to recover a stolen microchip.

Planners at IBDs, Wirehouses Earn Highest Salaries Among Advisors

It’s payday.

And even for financial advisors, where you work plays a significant role in determining how much you take home.

Advisors at independent broker-dealers and wirehouses were the industry’s highest earners last year, with median compensation (salary, bonuses, profit sharing) of $226,000 and about $214,000, respectively, according to the CFP Board’s latest compensation study. Advisors at big banks and hybrid RIAs fell in the middle, earning median compensation of $206,000 and $181,500. Advisors working at RIAs reported the lowest median compensation at $175,000. Not too shabby.

“While not necessarily surprising, the results reinforce that a financial planning career, and particularly being a CFP professional, is a rewarding career,” said Dr. Kevin Roth, managing director of research at CFP Board.

Making a Change

Compensation, however, isn’t the only factor advisors consider when choosing a channel.

The industry has experienced a steady wave of breakaway advisors leaving wirehouses and other large firms to launch or join RIAs. Chris Diodato, founder of WELLth Financial Planning, began his career as a dually registered advisor before dropping his Series 7 license and launching a fee-only RIA. Even though going independent meant potentially earning less, Diodato said the tradeoff has been worthwhile. “Being a strict RIA comes with operational perks, especially when it comes to compliance,” he told Advisor Upside. “Sure, I could make more money if I was dually registered, but I’d also have to spend significantly more on compliance or give up a portion of my revenue to a corporate RIA platform like Cetera or Raymond James.”

The Perks of Being a CFP. The report indicates the CFP designation, one of the industry’s most recognized credentials, comes with benefits beyond higher pay:

- Nearly 40% of CFPs engaged in profit sharing at their firms last year.

- About a quarter received elder and child care benefits.

- Some 60% have access to employee wellness programs.

The designation also correlates with job satisfaction, according to the Board. About 85% of CFP professionals described their careers as rewarding, citing stability, work-life balance and opportunities for advancement. Meanwhile, nine in 10 said they expect to remain with their current firm for at least the next two years.

Diodato, for his part, said the title “financial planner” should be reserved for professionals who have earned CFP certification, not, for instance, strictly insurance salespeople or those who just passed the Series 65 exam. “It dilutes the CFP mark when everyone is a financial planner,” he said.

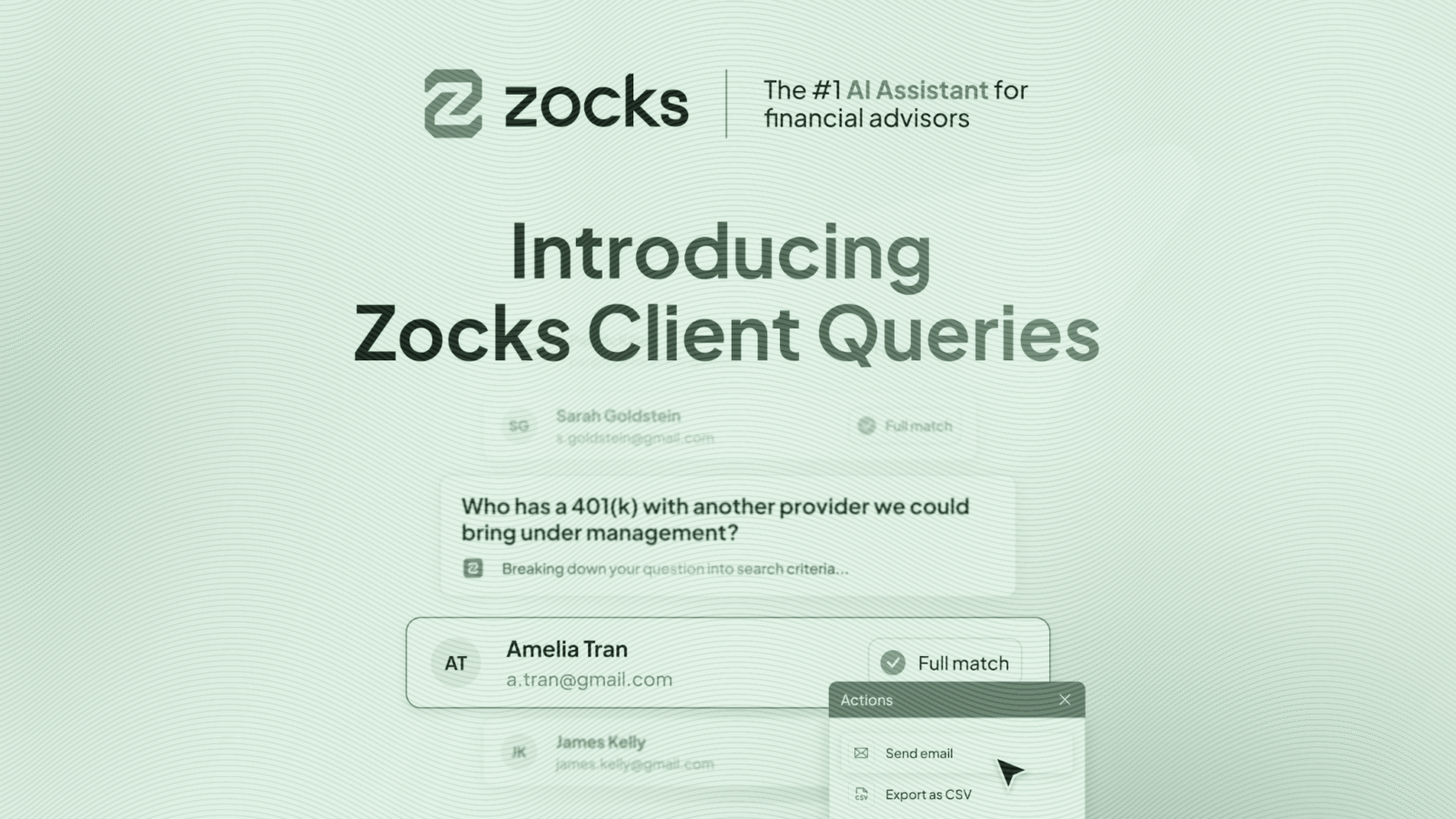

Your Client’s Money Isn’t All With You

Somewhere in your book…

- A client has an old 401(k) you don’t manage.

- A retiree holds a seven-figure account you’ve never seen.

- A new baby arrived, and nobody flagged the plan.

Miss them and the cost compounds — assets never consolidate, service gaps widen, and clients quietly take their money somewhere else.

You’d catch it in a full review, but those come once or twice a year. Checking records one at a time is just too slow.

Zocks Client Queries does that review for you instantly, reading across your CRM, planning data and every client conversation. Ask it like you’d ask a colleague, “Who’s sitting on held-away assets?”, and an actionable list comes back in seconds.

Clients May Have More Stashed in 401(k)s Than You Think

Give your clients a pat on the back.

Retirement savings rates and 401(k) account balances have reached record highs, according to Vanguard’s annual report published this week. The average account balance came in at $167,970, which is 13% higher than last year, while the median balance was $44,115, up 16%. Of course, average 401(k) balances don’t necessarily reflect total net worth, and are only a partial measure of retirement preparedness for most people. In fact, many people don’t have their money fully consolidated within view of their current advisor, so it’s worth asking what other assets might be out there that could be part of the overall plan. You know, your clients could be in even better shape than they look.

By the Numbers

More good news is that the account balances measured by Vanguard only show how much the approximately 5 million savers have accumulated for retirement with their current employer. When people change jobs or retire, their assets may remain with their former employer, be rolled over to another plan or an IRA, or be cashed out.

According to the report:

- One in four savers had an account balance of less than $10,000, while 35% of participants had a balance of more than $100,000.

- Eighteen percent had a balance of $250,000 or more.

Because of this skewed distribution of assets, average balances are indicative of savers at about the 75th percentile, meaning about 75% of people had balances below the average and 25% had balances above. Vanguard’s experts note that average balances are best understood as representative of the results experienced by longer-tenured, more affluent or older participants. The median balance, conversely, represents the typical participant.

What’s Behind the Growth? The average one-year total return for retirement plan investors was 19.3%. Among savers with account balances in both December 2024 and December 2025, the median account balance increased by 27%, reflecting strong positive returns in the equity and bond markets as well as ongoing contributions. Also helpful, nearly 70% of retirement plan investors now use professionally managed allocations, helping them build more diversified portfolios that reflect their time horizons and savings targets.

Could a China-Taiwan Conflict Crash Markets 50%? Sean Allocca and John Manganaro dig into one scenario that could break markets’ calm: a Taiwan invasion one expert projects could send markets down 40 to 50%. Plus: the psychology that trips up even rational clients near retirement, and a low-pressure way for clients to try retirement before committing.