AI Market Braces for Bellwether Nvidia Earnings Report

The US did approve 10 Chinese firms as buyers for the H200, Nvidia’s second-most powerful AI chip, though no purchases have yet been made.

Sign up for smart news, insights, and analysis on the biggest financial stories of the day.

Earnings at $5.5 trillion Nvidia are no longer just a simple update from head office, not when it’s the world’s most valuable company by roughly $700 billion (an Exxon Mobil’s worth, basically).

When executives report on its fiscal first quarter this Wednesday, markets will be looking for what the numbers tell us about semiconductor demand, capital spending by mega-cap technology firms, the near-term trajectory of the Nasdaq, the AI trade that is the engine of this year’s market rally and the fate of civilization generally. Okay, we made up that last one. Sort of.

Competitive Advantage

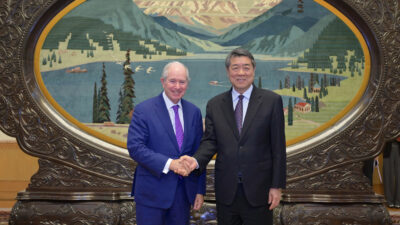

While CEO Jensen Huang was one of the powerful executives who joined President Donald Trump at a summit with Chinese President Xi Jinping last week, the meeting ended without any major deals. The US did approve 10 Chinese firms as buyers for the H200, Nvidia’s second-most powerful AI chip but, major caveat, Trump told reporters no purchases have been made because China is increasingly developing and relying on its own advanced AI chips.

There remains concrete business at home. Projected 2026 capital spending by AI hyperscalers like Alphabet, Amazon, Meta and Microsoft has risen from $531 billion in December to $725 billion, according to BNP Paribas, underscoring just how dramatically AI investment, which requires semiconductors, is accelerating. That means even if Nvidia cedes some of its roughly 85% market share to established competitors like AMD and Qualcomm, upstarts like the newly public Cerebras and hyperscalers launching their own chips, there’s still plenty of forecasted money to be made. Take the fourth quarter of its 2026 fiscal year, when revenue rose 73% year over year to $68 billion or the $78 billion forecast executives offered for this week’s report. It’s enough to mean that China doing its own thing and competitors finding their feet are unlikely to fluster bullish analysts:

- Wells Fargo forecasts Nvidia’s data center capacity will increase from 9.2 gigawatts in the previous fiscal year to 15.7 GW in the current one. They see annual data center revenue topping $500 billion in fiscal 2028 and $600 billion in fiscal 2029, and earlier this month, set a $315 target price for the stock. Bank of America analysts are even more bullish, with a $320 target.

- The Philadelphia Semiconductor Index, which tracks the sector, is up 64% this year, compared with Nvidia’s 23% advance, highlighting the explosive growth of rivals. But a more notable broader market concern is how both trounce the S&P 500’s 8.7%.

Seesaw: Still, there’s a lot riding on the immediate term. Depending on whether Nvidia meets or beats expectations, Saxo investment bank strategist Koen Hoorelbeke wrote that options traders are pricing in an 8% move in either direction for Nvidia shares. Buckle up.

Recent News

-

In AI Chip Race, Nvidia’s Biggest Customers Become Competitors

Photo illustration by Connor Lin / The Daily Upside, Photos by Hapabapa via iStock and Vincent Isore, Florian Gaertner, imageBROKER/Mojahid Mottakin, Andrej Sokolow, Wladimir Bulgar/Science Photo Library, and Kyodo via Newscom