Sign up for smart news, insights, and analysis on the biggest financial stories of the day.

Airbnb started in 2008 to facilitate a quintessential digital-age side hustle: Users renting out their homes for a weekend or two to secure the next month’s mortgage payment. But it soon became a gateway for creating real estate empires, turning neighborhoods into tourist zones and mom-and-pops into wannabe J.W. Marriotts — and upending entire housing and rental markets in the process.

Now the industry starts a new chapter: Workers are increasingly being ordered back to their offices. Meanwhile, cities and municipalities are passing sweeping laws to clamp down on your average multi-property owning mavens. Airbnb’s most recent earnings report included a less-than-rosy outlook for the rest of the year, and the company has launched a suite of new features that suggest it realizes it’s no longer the no-brainer cheaper alternative to traditional hotels it once was.

So was the success of short-term rentals a short-term phenomenon?

Checking In

Airbnb hit the Nasdaq in 2020 in the largest public debut of the year, giving the Uber-for-housing company a market cap of $47 billion. Today, it’s closer to $87 billion — around $30 billion higher than Marriott International and $47 billion higher than Hilton Hotels. Tech, and the adjacent side hustle economy it created, scales. The traditional tools of tourism? Not so much.

And while the pandemic caused hotels to suffer, Airbnb — with its reliable wifi and private rooms and private kitchens and, um, private air — soared:

- Airbnb actually posted a profit in 2022, its first ever, generating $1.9 billion in net income, the company reported. That’s well up from the $350 million loss it suffered in 2021.

- The company also reported 394 million “nights and experiences” booked in 2022, besting its record 327 million bookings from pre-pandemic 2019. Hotels, meanwhile, saw a 2022 nightly occupancy rate of around 63%, or roughly 5% lower than 2019 levels, according to data analytics firm STR.

Still, in its most recent Q1 earnings report, Airbnb said travel levels are likely to drop this year compared to the growth last year led by pent-up demand. How big will the drop-off be? Well, it depends who you ask.

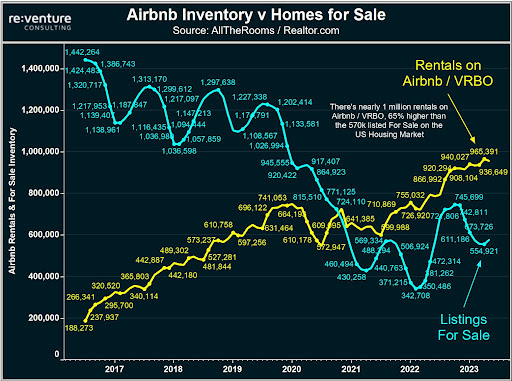

Data Concierge: If the short-term rental industry has a doomsayer, it’s Nick Gerli, CEO of real estate data analytics firm Reventure. In a viral tweet thread posted last month, Gerli, using data from short-term rental analytics firm AllTheRooms, noted what he saw as a bubble that’s already beginning to pop:

- In top Airbnb cities such as Phoenix, Austin, and Sevierville, Tennessee, revenue per available listing (RevPAL), a key metric in the hospitality industry, dropped nearly 50% in May 2023 compared to a year prior.

- “Ultimately this Airbnb crash was to be expected,” Gerli wrote. “The pandemic is over. Fewer people are working from home / vacationing in states like Montana, Texas, and Tennessee. So the demand is way down.”

That could spell trouble for the legions of new Airbnb hosts. While the company doesn’t publicly disclose a precise number of hosts, it said in its Q1 report that more than 4 million hosts use the platform and noted that, related to its mission to make hosting an Airbnb as mainstream as renting an Airbnb, total active listings grew 18% year-over-year. Gerli warned that many of these new hosts likely purchased their properties with mortgages saddled to much higher interest rates than those who have listed on Airbnb for years — creating the possible conditions for major market collapse.

Obviously, Gerli and Reventure’s business interests align with the perception of a rising real estate market. Though Airbnb’s public response to his claims didn’t exactly completely dispute them. “[Gerli’s] data is not consistent with our own data,” an Airbnb spokesperson recently told Bloomberg. “As we said during our first-quarter earnings, more guests are traveling on Airbnb than ever before, with nights and experiences booked growing 19% in the first quarter of 2023 compared to a year ago.”

That may be a bit of a non-denial denial. But other third-party analyses paint a slightly less gloomy outlook. Jamie Lane, chief economist and senior VP of analytics at short-term rental data analytics firm AirDNA, tweeted that its analysis does show a decline in RevPAL — only a much more muted one, around 5% to 10% depending on the market, than what Gerli found.

Stay A While: Whether or not Gerli’s projections are accurate, short-term rentals may well be cannibalizing many local housing markets. According to a study from The University of Pennsylvania’s Wharton School of Business, an increase in short-term Airbnbn rental listings in local markets is linked to a decrease in the supply of long-term rental units — likely leading to higher rents. That comes amid a nationwide dearth of new housing starts and home prices that rank among the highest in decades.

In many Airbnb hot spots, there are far more short-term rental listings than for-sale listings:

- In Phoenix, for example, there are roughly 18,000 listings for short-term rentals compared to just under 8,000 for-sale home listings, according to data from AllTheRooms and Realtor.com.

- In the Smoky Mountains vacation town of Sevierville, Tennessee, that disparity is even bigger — nearly 9,000 short-term rental listings compared to almost 900 for-sale home listings.

It’s easy to understand why property owners want to rent to vacationers. A short-term rental property in Sedona, Arizona, can generate as much as $60,000 in profit in a “crappy year” compared to just $30,000 for a long-term rental, according to a major property interviewed in a Wired feature on how short-term rentals have contributed to the city’s major housing crisis. That incentive structure has led to the rise of “professional Airbnb hosts,” individuals or organizations that buy up a portfolio of properties with the express purpose of renting them.

In fact, it’s this very housing market cannibalization that might lead to a significant regulatory backlash to Airbnb. In some major metropolitan areas, it’s already happening.

New York State of Mind: In New York City, a recently passed law would effectively put an end to professional Airbnb hosts altogether — outlawing any short-term rental property that isn’t also the host’s primary residence. The legislation could eliminate as many as 10,000 listings later this year. Denver has passed similar legislation.

The crackdown may already be affecting how Airbnb sees its future. In May, the company announced a new listing category called Airbnb Rooms — focusing on individual room rentals where guests stay with hosts and share common spaces, with an average nightly price of $67. CEO Brian Chesky billed it as a return to the company’s “soul,” harkening back to a more modest original vision of making travel cheap by cutting out the hotel industry’s monopoly. And it would conveniently offer a way to remain viable under conditions outlined in new laws like New York’s. It’s a full-circle tech story: a disruptor, now on top and facing increased regulation, is now finding a way to disrupt itself — and keep short-term rentals a long-term business prospect.