The Vanguard Patent Shaking Up the Fund Industry

Nearly 50 years ago, Vanguard disrupted the investing world by launching the first index fund for individual investors. Now comes the sequel.

Sign up for smart news, insights, and analysis on the biggest financial stories of the day.

Nearly 50 years ago, Vanguard disrupted the investing world by launching the first index fund for individual investors. Here comes the sequel.

Investors have tried everything to avoid paying those pesky capital gains tax bills in their mutual funds. Now Vanguard’s got an ETF share class for that — and by most indications, it could upend the $28 trillion fund industry.

The world’s second largest investment company after BlackRock, the Malvern, Pennsylvania-based Vanguard has experimented with a method for constructing exchange-traded fund share classes of its existing mutual funds over the past two decades. It’s been so successful that the company reportedly used the structure in 14 stock funds that booked $191 billion in gains for investors as of 2019 and paid out a total tax bill to the Internal Revenue Service of $0.

It’s a mouth-watering metric that took on even more significance after Vanguard’s prized patent expired last year. Now, Charles Schwab, Morgan Stanley, Fidelity, and roughly a dozen other companies have filed applications with the Securities and Exchange Commission to copy the structure. While it’s unclear whether the agency will approve the applications, its eventual decision holds enormous sway not only on the industry but also potentially over hundreds of billions of dollars in revenue for the Treasury.

“The SEC has been agnostic about the potential tax issue,” Fordham School of Law professor Jeffrey Colon told The Daily Upside. According to his research, the unrealized gains of distributed securities for the top 25 ETFs was estimated at $208 billion in 2020. The projected tax revenue at a common 23.5% tax rate topped approximately $50 billion in that year alone.

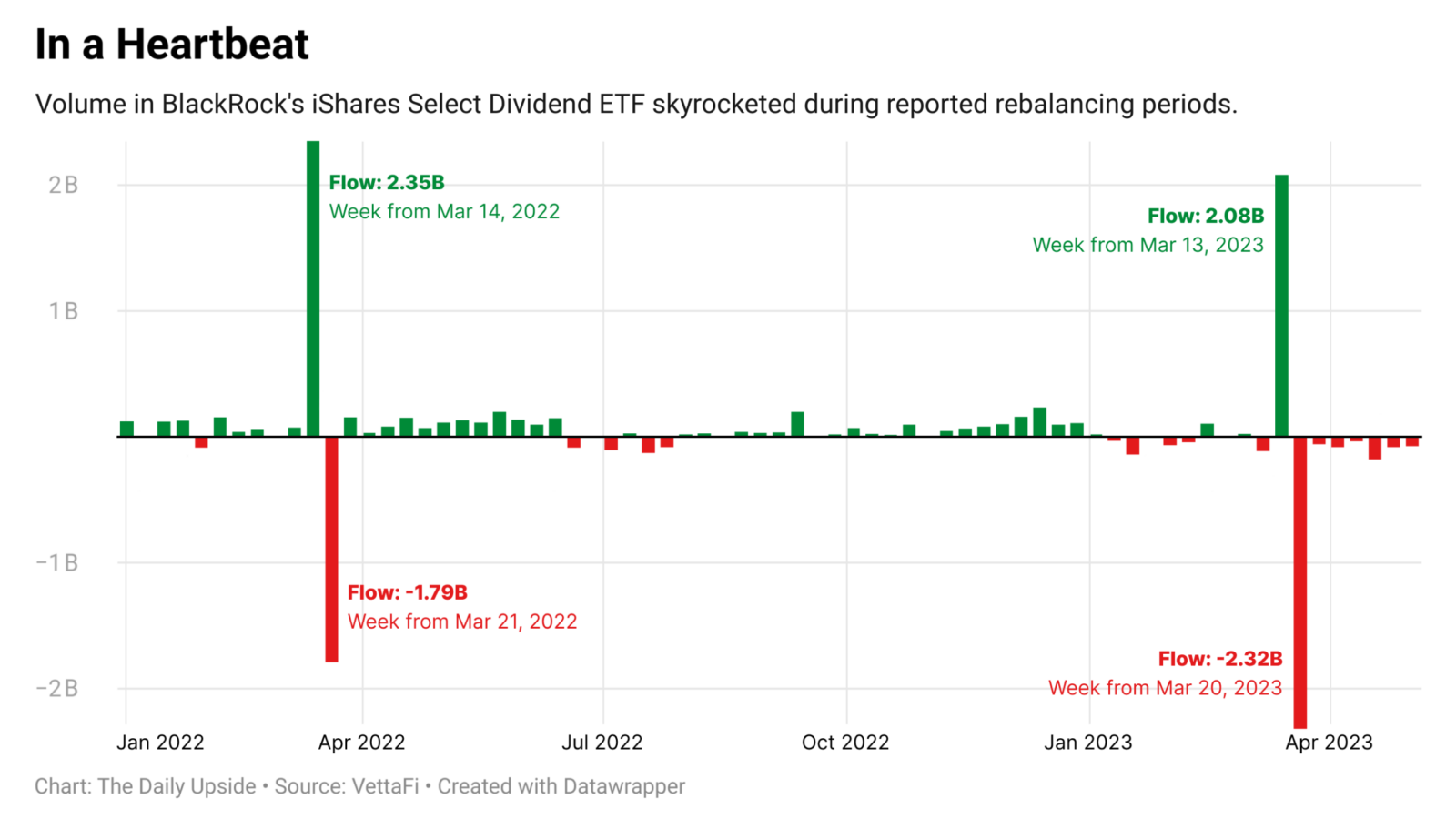

Checking For a Pulse

The secret sauce is in ETFs’ killer advantage over its big-brother mutual funds: taxes. Instead of buying and selling underlying securities, ETFs use a creation and redemption mechanism that adds or subtracts shares of certain stocks as needed. That means shares don’t necessarily have to be bought or sold, and don’t trigger capital gains — unlike mutual funds that report annual gains each year.

So-called heartbeat trades pump significant inflows into an ETF then quickly pull them out, which ends up looking like spikes on an EKG monitor to analysts (hence the name). By moving massive amounts of money in and out — often billions of dollars in under 48 hours — asset managers can essentially wipe away capital gains taxes by replacing highly appreciative securities with fresh ones. (A famous tax expert called it a “tax dialysis machine.”) It’s controversial, but a completely legal practice that is being used by most of the top names in the industry today.

ETF share classes could extend those benefits to existing mutual funds, with capital gains potentially stretching back decades. A nonpartisan congressional report that accompanied a Democratic bill to tighten taxes in 2021 estimated the government may be losing about $20 billion a year through similar practices, according to Bloomberg analysis. If the strategy is opened up to newcomers, that figure would likely climb.

“For more than 20 years, Vanguard investors have benefited from our multi-share-class structure,” said a Vanguard spokesperson, adding that the share classes are not removing capital gains. “While in-kind transactions can defer the realization of capital gains, they do not eliminate gains for investors.”

Death and Taxes

Another consideration is the other of life’s absolutes: death. If ETFs are held until the investor’s passing, the funds can be transferred to their heirs without realizing any capital gains taxes, much like other securities. Unrealized taxes add up to hundreds of billions of dollars for the IRS, and could become a potential stumbling block for mainstream acceptance by regulators, according to experts.

“It’s massive, just massive,” Colon said. “Almost no ETF has ever distributed capital gains and heartbeat trades allow them to do this indefinitely. There’s deferral while you’re alive and a step-up basis when you die.”

Baby boomers now hold more than $78 trillion in assets in the US, which accounts for about half of the country’s total assets, according to a Nasdaq report. While the majority — $41.8 trillion — is real estate, stocks and mutual funds are next in line with a staggering $33.8 trillion haul. “It’s a certainty people will die,” said FactSet’s director of ETF research Elisabeth Kashner, who was the first to coin the term heartbeat trades. “It becomes a question of what they’re holding — and when.”

For the US Treasury, it means a whole lot of tax deferral and not a lot of current revenue. When asked if other companies would likely take advantage of tax benefits if the applications are approved, Kashner was decided. “Why wouldn’t they?” she said. “Because it’s no longer subject to capital gains taxes, if that’s the case, it’s a deadweight loss for the Treasury.”

Buy Now, Pay Later While heartbeat trades have come under scrutiny in recent years, they’re nothing new. Proponents argue that most of the taxes are only deferred until the fund is sold, rather than avoided. It’s a slight but meaningful difference that leaves ETF investors on the hook for those tax bills later in life. The biggest ETF managers, including BlackRock, State Street, and Vanguard Group, all use heartbeats inside existing ETFs, according to Bloomberg. When an investor dies those capital gains are stepped up, but that’s true with many other investments.

Heartbeat trades have never been challenged in a court of law. In fact, the smartest minds in legal departments at asset management firms have gotten comfortable with the idea of helping their customers defer capital gains tax with heartbeat trades, according to Kashner.

“It’s an open question if the IRS ever decides to get more serious about it,” she said.

Sharing Is Caring Beyond tax benefits, there are also a handful of other advantages to the share classes. Most notably, ETFs help create more efficient and cheaper mechanisms for mutual funds that can bring down costs and make the funds much more appealing to customers. “If other asset managers can offer an ETF share class of existing mutual funds, the supply of ETFs will soar,” said Todd Rosenbluth, head of research at VettaFi. He added mutual funds will likely find themselves with a brand new investor base, and take advantage of their scale and existing track records.

The new class doesn’t work for every issuer. In fact, there are certainly downsides to becoming a transparent product like an ETF, which would result in daily holdings disclosures. For many funds, that’s just not viable, Rosenbluth said. “While this would be a key milestone, not all asset managers will want to offer ETFs, and certainly not for all strategies,” he said.

But most do. And they’re starting to really take off. A recent BlackRock report said billions of dollars worth of mutual fund assets are being converted into ETFs globally. Vanguard’s done it again.

Recent News

-

Photo illustration by Connor Lin / The Daily Upside, Photos by Shutter2U, Wavebreakmedia, and Feedough via iStock