Wall Street HALO Beckons Investors Trying to Ward Off AI-Driven Losses

As the AI bull run threatens formerly high-growth sectors like software, investors seek safety in HALO companies out of the tech’s reach.

Sign up for smart news, insights, and analysis on the biggest financial stories of the day.

In Renaissance art, halos are indicators of divinity and holiness, or at least spiritual enlightenment.

In financial markets, they have a more earthbound association. HALO, an acronym for heavy assets, low obsolescence, refers to a trade that confers a degree of immunity. Immunity from the potentially corrosive effects of AI on some assets, that is.

As the artificial intelligence bull run that’s lifted markets threatens formerly high-growth sectors like software with painful disruption, traders are seeking investments that can arguably sidestep or withstand AI and, in some cases, even benefit from it.

“HALO stocks are immune to Claude Code,” Josh Brown, the Ritholtz Wealth Management CEO, explained when he coined the term back in February. “Anytime people are freaking out about Claude Code and ripping capital out of the shares of its perceived gallery of victims, these are the types of stocks that are being bought instead.”

Apart from their perceived resilience to AI disruption, HALO companies often have little in common with one another, making them an unusual category, he added.

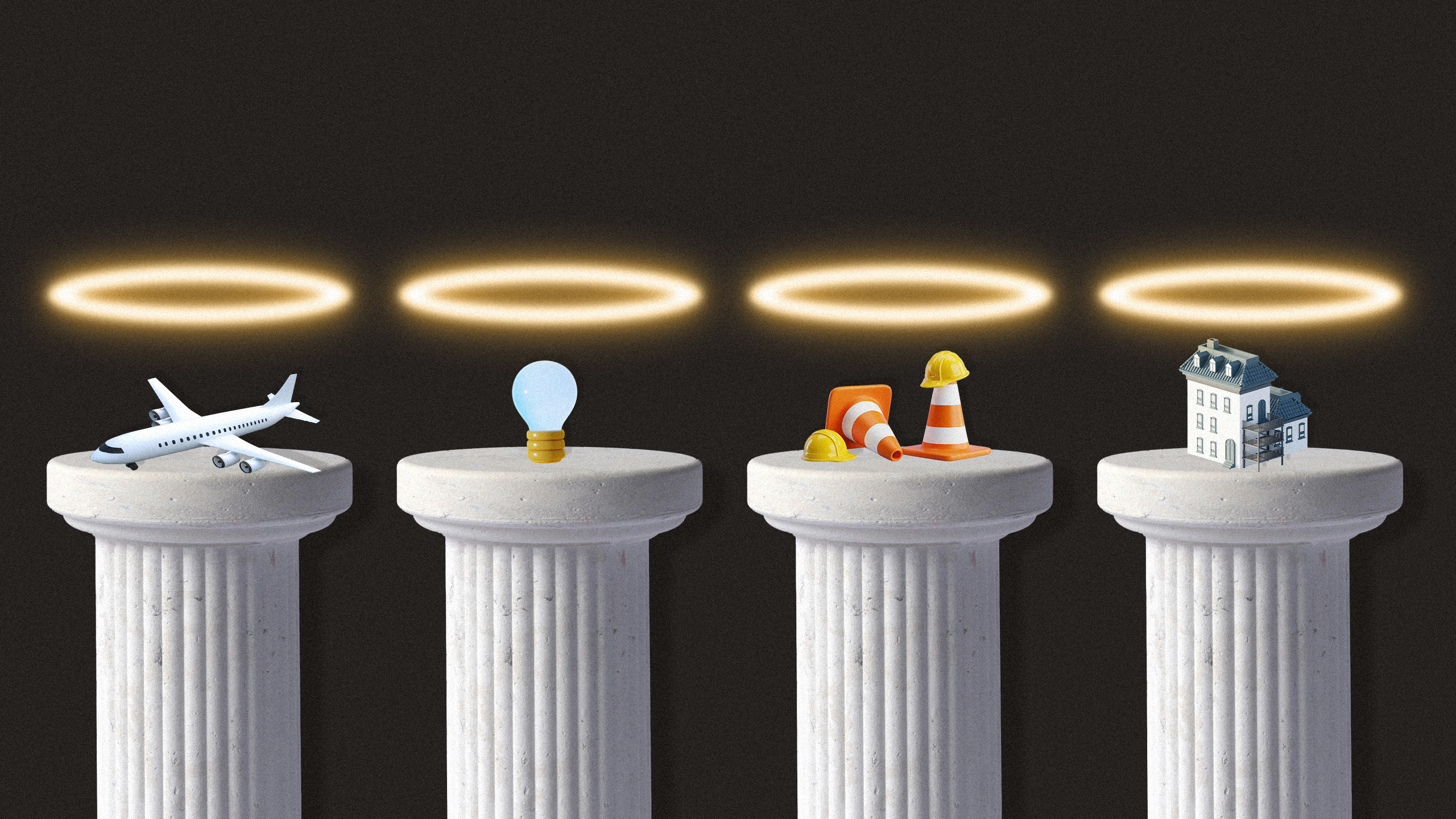

Heavy assets generally mean capital intensive businesses that need money up front, that use or manufacture machinery and that require physical property. For example, Enterprise Products Partners, up 19% this year, operates 50,000 miles of pipelines. Water utility H2O America, up 18%, operates 407,000 water and wastewater service connections.

Low obsolescence means something unlikely to be replaced by AI any time soon, like electric grids, air conditioners or Coca-Cola.

The opposite of this, what’s not HALO, are companies that are capital light, having minimal physical inventory or physical assets. Capital light firms, especially in technology and software, thrived in the era of zero interest rates and widespread liquidity in the decade following the Great Recession because they could raise money on the promise of rapid growth with little startup or maintenance costs.

The Costs of Going Light

“Technology companies and other capital light industries, which also took advantage of the expansion in the digital economy and smartphone usage, commanded persistent valuation premia,” wrote Goldman Sachs analysts. “By the early 2020s, this regime had pushed the MSCI Growth Index to more than twice the valuation of the MSCI Value Index.”

But recent years, even before the term HALO was coined, served as a reminder of just how valuable physical assets are. The post-pandemic inflation shock, oil market disruptions related to conflicts in Ukraine and Iran, and the Trump administration’s aggressive tariff regime pushed up the cost of capital, highlighting the importance of access to energy, supply chains and infrastructure.

Meanwhile, AI’s promise has added pressure on capital light businesses in technology and software. That’s because advanced agentic AI is poised to automate more workflows and coding, potentially eroding revenue models across entire industries such as software as a service (SaaS).

These factors have created conditions more favorable for capital intensive investments.

“The [return on equity] gap between capital light and capital intensive remains wide, but consensus forecasts now expect flat ROE for capital light companies, while capital intensive ROE is projected to improve,” Goldman’s analysts wrote.

Ritholtz’s Brown, in an effort to identify prominent HALO stocks, highlighted energy giant ExxonMobil (barrels of crude are “not going to end up in the crosshairs of DeepSeek”), retailer Walmart (“they have the best logistics network on earth, parking lots, stores, shelves, warehouses, inventory”), McDonald’s (you can’t code a Big Mac), and building materials producer Martin Marietta (“They make concrete. ChatGPT doesn’t and won’t.”).

There are also Hershey, Delta, NextEra Energy, Ventas and Caterpillar. All are HALO, one can argue, because even if an unprecedented AI model came out and proved the Riemann Hypothesis tomorrow, it wouldn’t replace Reese’s Peanut Butter Cups, Boeing 787 Dreamliners, the US power grid, retirement homes or bulldozers.

The most HALO-friendly sectors, Goldman said, include utilities, energy, telecom, airlines, and automobiles and auto parts.

Another beneficiary is real estate, according to analysts at Hazelview Investments, who noted real estate investment trusts outperformed the broader market in the first quarter.

“I’ve been in this business for over 25 years and, for many years, warehouses were just storage space; you’d go into a facility and see boxes,” says Rick Schaupp, a managing director at Clarion Partners, which oversees a $72.6 billion real estate portfolio spanning industrial, logistics, retail and apartments.

“Now, they’re the critical backbone behind the e-commerce supply chain and even supporting data center infrastructure and construction. Their strength lies in the fact that they are flexible, that layouts and design can change over time and reflect the different demand uses that we’re seeing and be part of the global supply chain network.”

Best Defense Is a Good Offense

While the HALO trade attempts to address the impact of AI on markets, it doesn’t quite fit the classic definition of defensive stockpicking, according to Roundhill Investments CEO Dave Mazza.

“Traditional defensives are often about stable demand and low earnings variability,” he wrote in March. “HALO is about something slightly different. It is about whether the core economics of the business are likely to be structurally disrupted by AI, or whether the company owns assets and networks that remain essential regardless of the next technology wave.”

That means HALO stocks don’t necessarily have to have classically defensive characteristics like steady earnings or dividends.

Mazza pointed to freight rail, which is cyclical due to its exposure to business cycles but is also virtually impossible to replace, as a sector with the requisite HALO qualities but not a traditional defensive profile.

Another quality that sets the HALO trade apart from traditional defensive positioning is that there’s an offensive element, too. Since the development and scaling of AI will require massive real-world assets and investments, companies that specialize in making and building them stand to gain.

There have been plenty of investor rotations into companies that stand to benefit. Shares in Vertiv, which makes cooling systems used by AI data centers, are up 86% this year. Comfort Systems, which specializes in heating, ventilation, and air conditioning installation and repair for server farms, is up 99%.

“The result is a combination of downside resilience and targeted offensive opportunity,” Peter Vanderlee, a portfolio manager at ClearBridge Investments, wrote of HALO stocks that “offer meaningful participation in structural growth themes.”

With AI hyperscalers set to deploy some $765 billion in capital spending this year and $1.6 trillion by 2031, according to Goldman estimates, that’s a lot of offensive opportunity for companies that specialize in real-world infrastructure to capture.

It’s also why memory and data storage giants like Micron Technology, Samsung Electronics and SK Hynix are considered HALO candidates. Or chipmaker Taiwan Semiconductor Manufacturing Corp. and photolithography machine manufacturer ASML.

All of them have sophisticated, advanced infrastructure that is unlikely to be replicated, and their products are crucial to scaling AI.

Old School Assets, Old School Problems

The virtue of HALO companies also explains their potential downsides. Heavy assets mean operations that require significant, ongoing capital expenditures and the maintenance and upgrading of infrastructure.

Real-world assets mean real-world problems: Earnings can take a hit from higher construction costs resulting from inflation, disruptions to supply chains, labor shortages and time-consuming regulatory approvals that hold back projects.

Many companies also rely on debt to fund and sustain their real-world footprint, which can make them sensitive to interest rates and fluctuations in credit markets.

Ultimately, that means the HALO trade will require thinking beyond sectors. Instead, investors will have to identify the companies that are the best at executing plans.

Recent News

-

Photo illustration by Connor Lin / The Daily Upside, Photo by Frentusha via iStock

-

Photo illustration by Connor Lin / The Daily Upside, Photos by Shaina Benhiyoun, Weston Hancock, Erica Denhoff, IMAGO/JOERAN STEINSIEK, and Kenya Sumiyoshi via Newscom